Keysight, Much Better than the Drop Would Suggest

Q1 2025 Earnings Digest

Keysight reported its first quarter as a portfolio company this week. Although the market reacted negatively to the company’s earnings (almost a 7% drop), I must say that I believe there were more positives than negatives in the release:

The reality is that not much changed in Q1 compared to what management shared in Q4. The environment is improving, and significant optionality from M&A remains (I’ll discuss this in more detail later). I am still building my position in the company, so I welcome any drops as long as the business isn’t fundamentally changing.

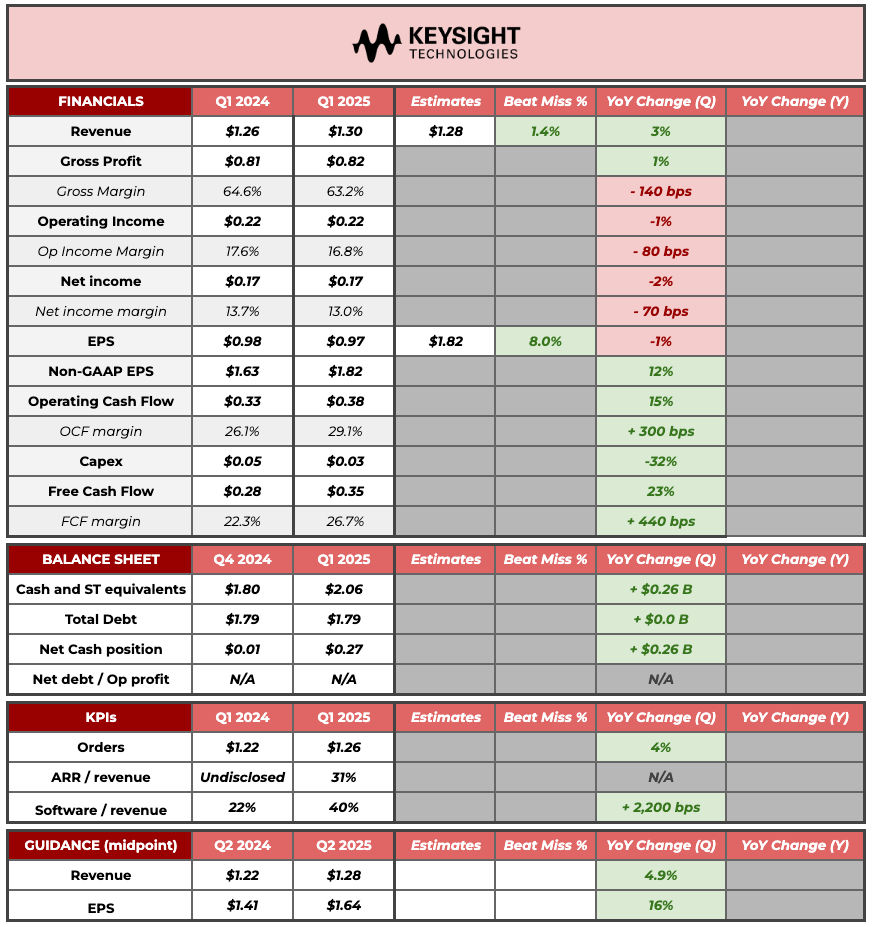

In this article I’ll make a “quick” overview of the quarter and share some thoughts on valuation. Let’s start with the summary table for Keysight.

The first thing that should stand out is that Keysight has passed the cycle's trough (90%+ likelihood this is the case). The company enjoyed its first growth quarter since July 2023, and year over year growth is expected to accelerate in Q2 (note that comps get easier in Q2 and Q3). The chart below is the textbook example of a company coming out of a downcycle: