Judges’ Scientific (JDG.L): Time to do something

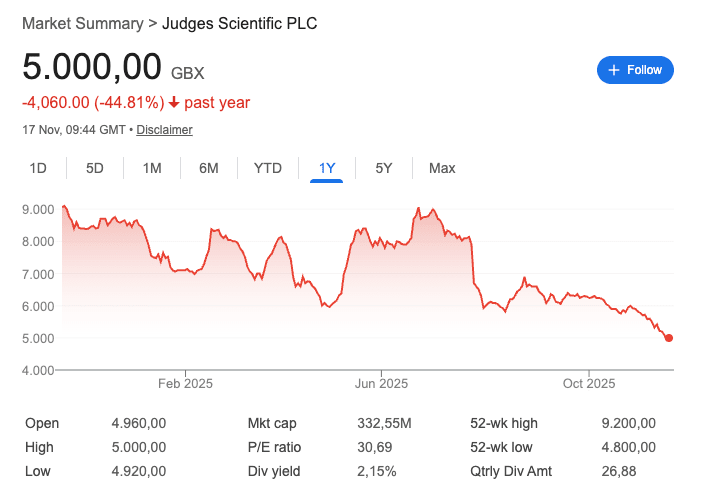

You might have noticed that Judges’ stock is considerably down over the past few months. Despite already being somewhat cheap at the beginning of the year, the stock has taken an additional 45% haircut:

Even though the additional drop from what apparently seemed like an attractive level might suggest that Judges’ stock has gotten “unjustifiably” cheap, we must not forget that several things have changed for the company this year, and we must account for these to make an apples-to-apples comparison.

I covered most of these in my last article on Judges, but I thought it would be a good idea to summarize them here. Judges has faced several headwinds simultaneously in 2025:

Challenges with university funding in the US driven by the Trump administration

Organic challenges at some subsidiaries

Weak pace of capital deployment (no acquisitions over the last 15 months)

The admission by management that there might not be a coring contract in 2026 (still TBD)

Let’s go over these one by one.

(a) Challenges with university funding in the US driven by the Trump administration

I don’t know how secular this will be, but considering that Judges’ has to an extent derisked this part of the business (by assuming that orders don’t come back), I would say that most of the impact has already been felt. Several universities are already reaching deals with the US administration or winning in court. Even if the “new” environment is still significantly below “peak funding,” there are reasons to believe this will be additive to Judges’ growth from currently “derisked” levels. In a recent call, Bruker mentioned that their academic and government segment had been driven by ex-US orders, with the US environment remaining weak but stable. The word stabilization has appeared across many companies exposed to US university funding, which is encouraging.

Recall that, during its most recent call, Judges’ management admitted to not knowing when these headwinds will fade, but that they are repositioning their businesses to cater to the industrial segment in the US, which is much larger. This means that, if successful, Judges should theoretically be able to grow if these headwinds prove to be more secular than temporary. What does seem obvious is that management has taken a conservative stance on this topic.

(b) Organic challenges at some subsidiaries

These challenges are unrelated to US university funding challenges, but they are important nonetheless. Management views these as temporary and is working to solve them. Judges has historically enjoyed a 7% organic growth in sales CAGR (even after the recent drop), but I don’t believe the current valuation assumes this is a sustainable level.

(c) Weak pace of capital deployment (no acquisitions over the last 15 months)

This honestly doesn’t worry me much, because all good capital allocation is lumpy. Management has recently hired Rik Armitage to accelerate capital deployment, but remains committed to making acquisitions only when they make sense. Expanding the M&A team definitely helps with the top of the funnel and should eventually lead to more acquisitions without sacrificing the strict M&A criteria.

One thing that seems interesting is that Judges is not finding more M&A candidates during this period of turbulence. David Cicurel once mentioned that owners don’t tend to sell their businesses when they believe the weakness is transitory, and that might be the case right now.

Note that this adds fuel to the fire, because Judges historically grew organically during periods of somewhat weak capital deployment, but this is not the case right now (excluding the Coring contract).

(d) The admission by management that there might not be a coring contract in 2026 (still TBD)

This is an important and undiscussed topic from the most recent call. Management shared, out of the blue, that they did not know whether there would be a coring contract in 2026. This is pretty relevant because a Coring contract typically generates around 6 to 7 million pounds of EBIT and, therefore, is a significant contributor to consolidated EBIT.

Note that, even though Judges is having a tough year, it’s still growing. The reason is that 2024 numbers were all but normalized. No Coring contract in 2026 could mean that the most significant growth tailwind to the numbers this year turns into a headwind. All this said, all the weaknesses in the non-Coring business might be enough to offset the absence of a Coring contract (albeit this is TBD).

So, all in all, not a great year for Judges, with the Coring contract even masking a good portion of the real weakness the company is experiencing.

Why the need to make a decision?

Given that many of the headwinds above are potentially temporary, we must assess the current valuation to determine whether Judges is still a buy here. Before doing this, let me explain what led me to revisit my position. Several months ago, I published this article in which I claimed that, to avoid complacency, I would implement a rule to sell or add to a position when it was considerably down from my cost basis. The reason behind this strategy was basically to force myself to do something. In my view, there are only two potential scenarios when a stock is down considerably from our cost basis…

The moat and business quality have been significantly eroded, and therefore a sell is warranted regardless of the price (i.e., the market was, to an extent, correct)

You are getting a similar company for 30% less than the price you thought was attractive in the first place (i.e., the market is extrapolating the recent weakness to the future)