Is Danaher wrong with Masimo?

Unpacking the $10 billion acquisition

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join hundreds of subscribers today:

Danaher announced last week its intention to (still pending regulatory approvals) acquire Masimo Corporation (MASI) for $180/share paid in cash (total deal value of $9.9 billion). This makes Masimo Danaher’s third largest acquisition ever, only behind Pall (2015) and Cytiva (2020). The market did not react positively to the news initially (Danaher’s stock was down 3% the day of the announcement) but the question investors should try to answer here (irrespective of market reactions) is…

Is this a good asset?

How does it fit strategically?

Is the price paid reasonable?

Let’s start by understanding what Masimo does.

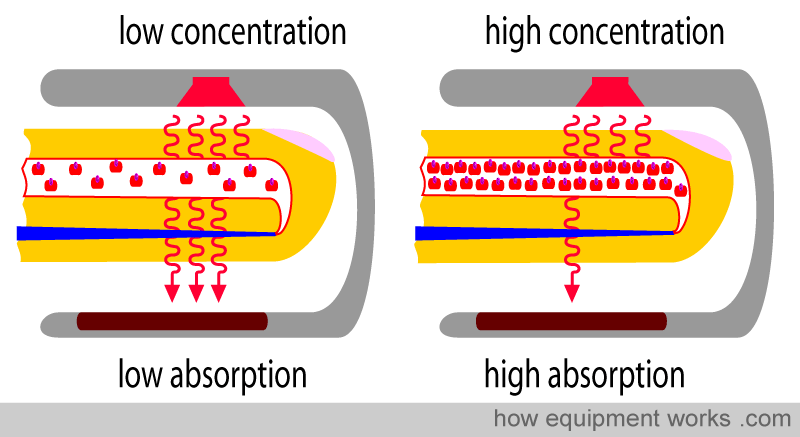

Masimo is the market leader in non-invasive pulse oximetry. This sounds fancy, but it’s simpler than it sounds. Pulse oximetry is the process used to understand the oxygen concentration within the blood. The process requires a pulse (evident by the name), which is why it’s measured with the arterial flow rather than the venous flow. The process underlying pulse oximetry is called spectrophotometry. Different light wavelengths are sent through the patient’s tissue. To know how much oxygen there is in the blood, one simply has to calculate how much light is absorbed by the sensor:

Traditional pulse oximetry faced several challenges stemming from patient motion (a patient moving their hand and leading to venous flow to move and distort the numbers) and low perfusion (the artery signal quieter than usual). This led to a significant number of false positives and negatives. We are talking about diagnostics here, so false positives and negatives could lead to severe patient complications.

Masimo developed a technology to solve this: SET (Signal Extraction Technology). SET uses spectrophotometry (like traditional pulse oximetry) but uses complex algorithms to eliminate the noise that led to false positives and negatives in the traditional process. SET is very superior to the traditional technology and comes with several benefits to hospitals/practitioners:

It can reduce false alarms by up to 90% (so nurses become more efficient)

Allows for continuous monitoring because motion is not a problem anymore

It allows for much more accurate blood monitoring in neonates (that tend to move quite a bit)

Despite SET being a disruptive technology, it’s not new. Masimo introduced SET around 1995, and while it has lost patent exclusivity on the first iterations, the company has developed several other iterations whose patents expand beyond 2028. One of these is the rainbow platform.

Masimo’s goal with the rainbow platform was to expand SET into additional indications. Traditional SET technology was based on two wavelengths and focused specifically on oxygen. The rainbow platform uses between 7-12 wavelengths and can analyse the entire spectrum of blood components simultaneously. Rainbow was launched in 2005, but recent activism has made management focus increasingly on it.

Now that we know what Masimo does, it might be interesting to understand how it makes money. Unsurprisingly, it’s a razor-razorblade model. The company sells the razor (its platforms like Radical 7 and Root) at a low margin, but this razor comes with a long-term stream of high-margin consumables. In Masimo’s case, consumables are single-use sensors used in pulse oximetry.

Interestingly, Masimo’s business appears to be better than “just” a simple razor-razorblade model. The reason is that a good chunk of Masimo’s hardware can be upgraded immediately to rainbow configuration, but this upgrade requires a software license. This software license was one-time in the past but is now becoming recurring revenue. This means that Masimo makes money when the hardware is sold (one-time sale and cyclical), when consumables are used (recurring business), and when the hardware is upgraded (somewhat recurring). This said, Masimo doesn’t disclose specifically how much software revenue they generate.

We also have to consider that Masimo also benefits from price-mix tailwinds. Once the hardware has been upgraded to rainbow, sensor ASPs (Average Selling Prices) increase around 3x-5x. Why? Because Rainbow sensors are significantly more expensive than “oxygen-only” sensors. The good news for Danaher here is that the runway for the rainbow platform seems pretty substantial, adding around 2-3% to the long-term growth algorithm:

As we look across our market opportunities and how this translates into kind of the straight math, we really have a long runway for growth. ... Growing in advanced monitoring [Rainbow] is about one-third of our [7% to 10%] growth.

So, ultimately, Masimo is a business with 80%+ recurring revenue that grows at a HSD clip organically and enjoys good margins:

The source of these financials is Masimo’s technological superiority which has made the company prevalent across US hospitals: Masimo’s SET technology is being used in 10 out of the top 10 hospitals in the US.

Now, if this is the case, one could ask themselves why is Danaher able to acquire Masimo at an okay price despite paying a 40% premium (i.e., why was the stock cheap?). That’s a question that I’ll go over later.

Masimo’s two uncertainties

Masimo comes with two uncertainties (obviously I don’t expect Danaher to be blind to these); one good and one “bad.” Let’s start with the good: the Apple lawsuit. In 2023, the ITC ruled that Apple had infringed Masimo’s patents. Apple had theoretically used Masimo’s SET technology on the Apple Watch. This ruling eventually led to a discontinuation of Apple’s blood oxygen feature over a period of time.

The story continued in 2025, when a jury in California found Apple liable for infringing Masimo’s patents. Apple supposedly used Masimo’s patented technology in around 43 million Apple watches sold between 2020 and 2022. The judge ordered Apple to pay $634 million in damages to Masimo. The outcome, however, is still uncertain. Apple worked on a workaround and the ITC is analysing if this workaround still infringes Masimo’s patients. Apple also appealed the California jury decision, so we still don’t know what will happen.

Now, as a Danaher shareholder I think it’s worth assuming that Danaher gets $0 from this, but there are several potential pathways here. If there’s wrongdoing here (still TBD), I see two options for Danaher:

To continue with the litigation. Let’s not forget that Danaher likely has more resources to fight Apple in court.

To reach an agreement and sign a licensing deal with Apple.

We don’t know which one it’ll be, but it does seem that whatever the outcome it’ll probably be positive. As I stand today I would argue that #1 is unlikely because Danaher’s management likely doesn’t want anything to distract from the integration process, but we’ll see.

We could consider the other uncertainty negative. Masimo has always been a good asset, but it has historically faced governance problems led by its founder Joe Kiani. The last straw was Joe Kiani’s decision to acquire Sound United, an audio-brands company totally unrelated to Masimo’s core business, using $1 billion of the company’s cash. Masimo’s stock fell 30%+ the day this was announced.

Kiani was well aware that shareholders would want to fire him for such a move, so he “secured” his spot by establishing a $400 million payout in case he got fired after a board takeover. This didn’t stop Politan Capital (an activist investor) from taking two board seats in 2023 and making an attempt to fire Kiani in 2024. This first push was unsuccessful, but Kiani eventually resigned in September 2024, not without drama though. Kiani argues that they owe him hundreds of millions from his termination package and Masimo alleges that they fired him for cause and that, therefore, he is not eligible for the payout.

Both uncertainties seem to net out, but I believe the outcome will not be that relevant for Danaher’s returns.

The strategic fit (this is what ultimately will matter)

Regardless of Masimo’s quality as an independent asset, we must try to understand why it’s more valuable within Danaher than it is as a standalone business (or why it’s not). Let’s talk about synergies. One thing I will say is that I did not particularly like seeing Danaher talk about revenue synergies in the press release. Not because they are not going to be achieved (they likely are), but because a deal should never be based on revenue synergies. With this said, let’s start with these.

The main revenue synergy will most likely come from the combination with Radiometer. Danaher acquired Radiometer in 2004, a company which specializes in acute care diagnostics primarily through Arterial Blood Gas. ABG is an invasive procedure because the objective is to get a lab-quality measurement of blood parameters. It might seem that both Masimo’s SET and Radiometer’s ABG overlap, but they seem to be quite complementary and allow Danaher to offer the E2E (end to end): owning Masimo for continuous monitoring and Radiometer for the lab-quality tests. Owning both companies allows Danaher to pitch an E2E solution to hospitals and also allows significant cross-selling.

Another interesting topic is global cross-sell. Radiometer has its roots in Copenhagen and is much more prevalent in the EU and Asia than Masimo is. On the flipside, Masimo is very prevalent in the US but not so much in international geographies.

This means that Danaher can potentially use its Radiometer salesforce and customer relationships to sell Masimo in international markets. This E2E pitch should allow Masimo to gain an advantage against Medtronic, which acquired Nellcor (Masimo’s Pulse Oximetry rival) in 2015.

Despite revenue synergies being evident, the “safest” synergies (and the one we should count on) are cost synergies. Danaher made the following claim in the press release:

Danaher expects to realize more than $125 million of annual cost synergies and more than $50 million of annual revenue synergies by the fifth full year following completion of the acquisition.

There are evidently manufacturing and SG&A synergies once Danaher plugs Masimo into its Diagnostics platform, and we shouldn’t forget about DBS. Danaher typically expands the operating margins of acquired companies significantly post-DBS implementation (note that the margin expansion can’t be exclusively attributed to DBS because there are duplicate costs taken out as well). Let’s look at some examples. In the most recent earnings call, management discussed that Abcam’s operating margins had been improved significantly post acquisition:

I mean, we’re really encouraged by what we’re seeing here at Abcam. The business continued to improve here in the fourth quarter. In fact, we’ve seen now three months of growth, particularly driven by the recombinant protein in the pharma segment that we’ve been talking about. And of course, the team has been working very hard on right sizing the cost picture there to the business and to our earnings expectations going forward. And we see that. In fact, the operating margins are 500 basis points higher than when we acquired the business, and so we like what we see here for Abcam and expect to continue to see that trend here in 2026 as well.

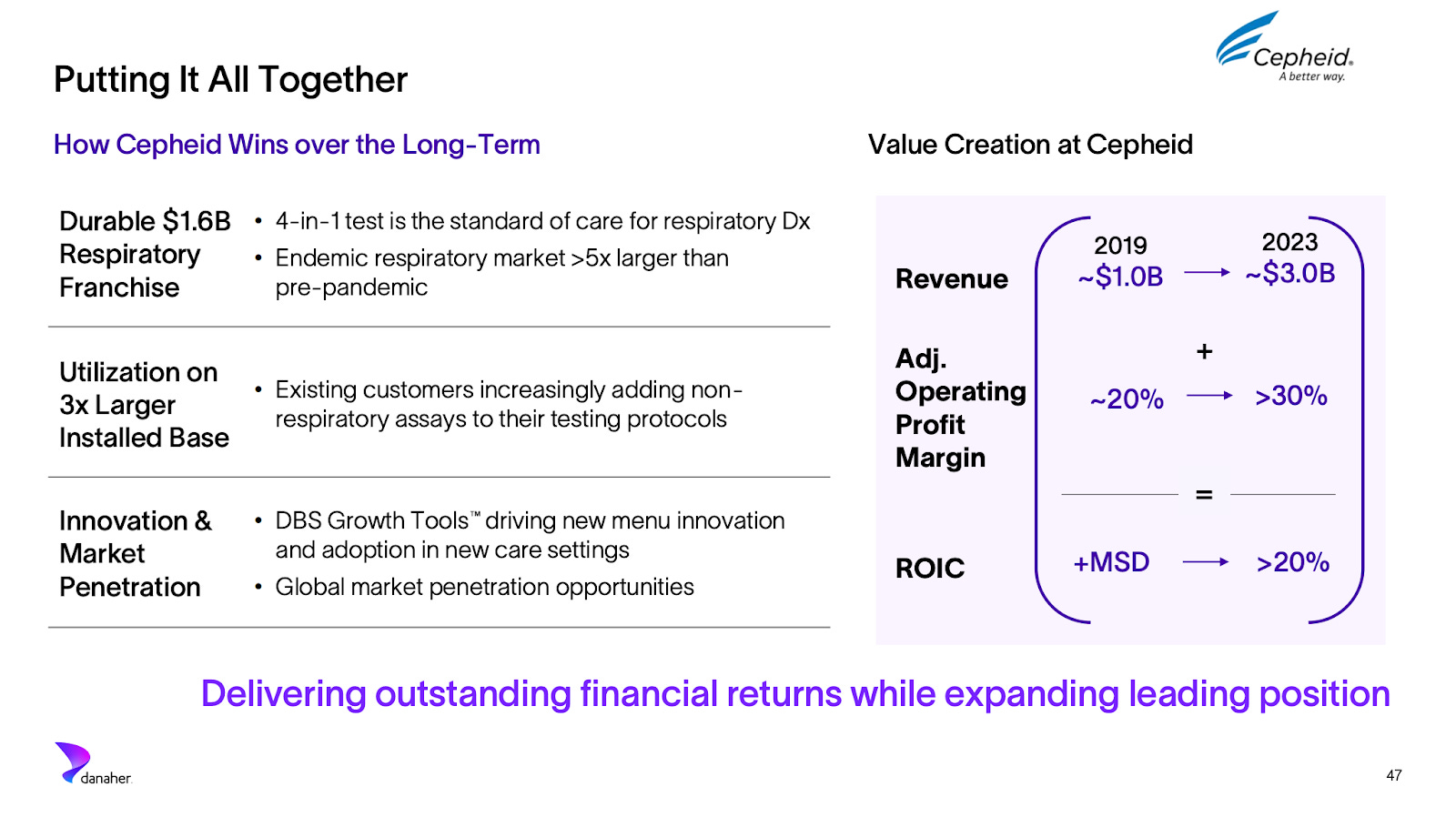

Cepheid enjoyed a similar fate. Cepheid had breakeven operating margins when Danaher acquired it in 2016. Operating margins had risen to 20% by 2019 and eventually reached 30%+ in 2023. This margin expansion, by the way, did not come at the expense of growth/innovation:

Should we expect something Cepheidesque in Masimo? Probably not to the same degree, but it’s undeniable that the DBS playbook has worked well for Danaher time and time again. Cepheid is a particularly interesting case because the Cepheid/Beckman Coulter synergies are somewhat similar to what Danaher might experience between Radiometer and Masimo.

All in all, not only is Masimo a good standalone asset but it also seems like a good strategic fit for Danaher. It’s important to note that Masimo did not suffer from operational problems (other companies Danaher has acquired did), it suffered from governance problems which are likely to disappear under Danaher’s leadership. It’s an asset that makes a lot of sense for Danaher because (1) it allows the company to deploy significant capital, (2) it’s acquired at a relatively okay valuation (more on this in a bit) and (3) it makes strategic sense and is a repetition of a playbook that Danaher has applied before.

Is it a fair price? (and what the market probably dislikes)

The final missing point here is whether the price paid for Masimo is fair. This is something we will only know in hindsight, but I’ll give it a shot. Let’s start with the price tag. Danaher agreed to pay $180 per share in cash. This means that it’s paying around $9.9 billion for Masimo. The company expects that, under Danaher’s ownership, Masimo is going to generate an EBITDA of at least $530 million in 2027, which means that Danaher has paid around 19x next year’s EBITDA (pre-synergies).

Masimo’s long term growth algorithm calls for revenue growth between 7-10%. If we assume some kind of revenue synergies we could argue that Masimo under Danaher will grow closer to the high end (if not above) of this range, so let’s say 10%. Masimo also guided for operating margins above 30% in 2028. If we add 300 basis points coming from cost synergies and DBS, we conservatively get to 33% operating margins in 2028. This means that, under Danaher’s leadership, Masimo could potentially generate EBIT of $670 million by 2028, for a 15x 2028 EBIT multiple.

We don’t know what Danaher will surprise us with in terms of growth and margins (Masimo was not counting on a lot of international growth to get to their LT construct), but it does seem like a relatively expensive asset (although definitely much cheaper than Aldevron!).

What the market doesn’t like (and I can somewhat understand)

I believe the market is not worried about the asset and the multiple paid, but rather about the fact that it somewhat obscures Danaher’s bioprocessing exposure. Bioprocessing is considered the highest quality segment in healthcare, so everyone wanted Danaher to deploy capital but to deploy it in bioprocessing. With Masimo, Danaher is deploying capital in diagnostics, which is not a bad business (and Masimo is not a bad asset) but it’s not bioprocessing. I get the point, and it somewhat makes sense.

My pushback would be that it would pretty much be impossible to acquire something decent in bioprocessing at a decent multiple. Note that Danaher’s combination of Pall and Cytiva (the two largest acquisitions in the company’s history) also allows the company to sell the full stack, so it’s not like it needs any tuck in. Now, what about buybacks?

Danaher is currently trading at a forward EBIT multiple around 19x (assuming adjusted operating profit grows 10% in 2026), so it’s likely cheaper than Masimo is (albeit also growing slower). Wouldn’t it had made sense to deploy more capital in buybacks and not acquire Masimo? The market seems to agree with this because it would’ve also allowed to keep a cleaner bioprocessing exposure while reducing the share count, but we’ll see what is a higher return endeavour going forward.

I still have a lot to learn about Masimo and how it fits within Danaher, but at first glance it doesn’t seem as dramatic as many have pointed out to be.

Have a great day,

Leandro

Has Danaher talked about financing for the deal? $4b of cash on hands. BS is not overleveraged, but this will push leverage likely towards 3x net debt/EBITDA is the math in my head is correct. I'm still not sure if I am much of a fan of buybacks at Danaher.

Sartorius is also starting to look interesting again as a purer play on Bioprocessing (lower quality management however).