From headwinds…to tailwinds

Judges Scientific's 2025

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

You can find Judges Scientific’s in-depth report here:

Join hundreds of subscribers today:

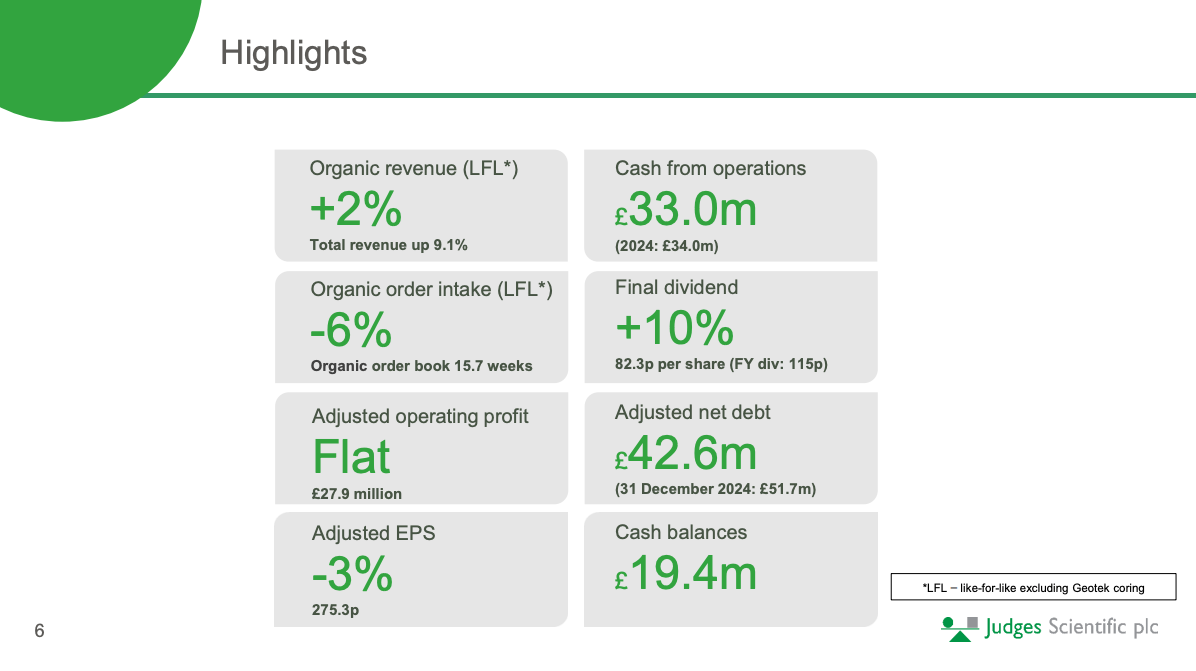

Judges reported (as expected) soft 2025 earnings this week. The “rest” of the business was only just enough to counter the impact of the university funding freeze in the US. Revenue grew 2% organically (excluding Geotek) but orders and profitability struggled:

Source: Judges Scientific

Note that the first half of the year was okayish, with the “severe” problems beginning in H2. This ultimately means that the business will still suffer tough comps in H1 2026 (currently experiencing a 17% drop in orders), but that comps should start to moderate significantly as the year progresses. Management decided to reset expectations back in January when they reported the preliminary results, something that is also coherent with the fact that the company has a new CEO. They now expect adjusted EPS of 225 pence at the midpoint in 2026, which would result in an 18% year over year decrease. This guide, however, includes two important assumptions that should theoretically mean that it “can’t get worse” (famous last words?):

The guide doesn’t include a Coring contract

The guide doesn’t assume any improvement in the US funding environment

Let’s discuss these two assumptions in a bit more detail, starting with Coring. Management shared that they expect a Coring contract early 2027 and that their expectation now is that they’ll have 3 Coring contracts every 4 years. This, in my view, is good news, or at least good news for me as I expected 1 Coring contract every 1.5 or 2 years. 3 Coring contracts every 4 years means that Judges now expects one Coring contract every 1.33 years (not terrible). Management also noted that their confidence in this new estimate is relatively high because they are in close contact with the few Coring customers (Japan, India, US, and China).

Interestingly, management also noted the following in the earnings report:

Separately, the 2024 parent company balance sheet has been restated to reverse an impairment of £8.3m in relation to the parent company’s investment in Geotek. The 2024 impairment was recorded following the auditor’s stress testing of the Group’s value in use calculation. In hindsight, the auditor’s stress testing was too prudent and therefore the impairment was not required. The effect of the prior year restatement is to increase 2024 net assets of the parent company by £8.3m and the parent company income statement by £8.3m. This has no impact on the Group’s results as reported.

Despite not having an impact on cash flows or the current year’s numbers, I believe this restatement is pretty significant. If there’s one thing that shareholders were worried about (besides university funding in the US), it was that Judges might have made a mistake in acquiring Geotek, something that would’ve proven significant considering it was the largest capital deployment in company history. All in all, I’d say that 3 Coring contracts and 4 years and the reversion of the Geotek impairment should serve to calm investors regarding the investment. Now, even though the Coring contract in 2025 served to tame the impact of the reduced university funding in the US, this contract will be non-existent in 2026. This means that things could get worse from 2025, and they did! This, however, should mark the bottom of the cycle for Judges (hopefully).

As in relation to point #2 (university funding in the US), management claimed that (while not taken into account in the guide) they are seeing some green shoots. The key unknown, though, is timing:

We’d also highlight that uncertainties remain around U.S. federal funding. Since our January trading update, the U.S. Congress has approved the next round or the 2026 budget for U.S. funding of scientific or academic research. That funding was restored to prior levels, there or thereabouts. We see that as really positive news insofar as the opposite would obviously have been very negative news. At the moment, there remains uncertainty around how the funding will actually flow.

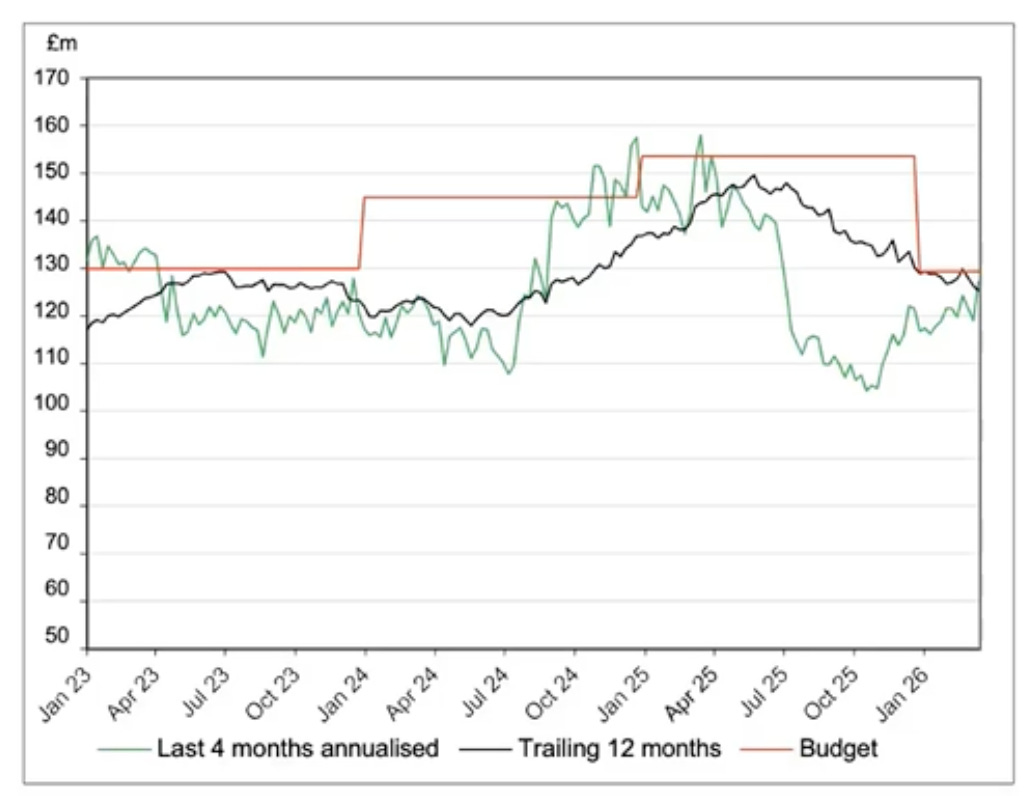

It’s anyone’s guess when the restored funding will flow into universities and when these universities will decide it’s time to set new orders, but from our point of view (as shareholders) we should see this as great news for the sole reason that it’s turning from a headwind into a potential tailwind/source of optionality. Once H1 is said and done, comps start to soften and this part of the business has pretty much gone to 0. This means that any incremental improvement should be good for Judges. This is still TBD (to be determined), but things seem to be pointing in the right direction thus far with orders somewhat starting to recover (green line):

I believe that the market is interpreting these two points as an admission that the 2026 adjusted EPS number is indeed consistent with the bottom of the cycle. With Judges trading at 19x bottom-of-the-cycle EPS, I’d say the risk/reward on the shares seems attractive here. Note that, even though a recovery in orders related to improved university funding was not taken into account in the guide, management believes these orders could come at any moment…

As Brad mentioned earlier, it’s worth reminding that that is relative to our strongest period last year. It’s also worth mentioning that it’s still early during the year.

At 17%, it could be a couple of instrument orders or a stocking order from an OEM or a distributor that could shift that percentage by a few points either way.

Another growth lever that management is not taking into account in the guide (logically due to its lumpiness) is acquisitions. I believe Judges is currently experiencing one of the longest (if not THE longest) periods without conducting an acquisition. The company’s last acquisition took place in August 2024 (Teer Coatings). This acquisitive drought has coincided with one of the longest droughts in terms of organic growth, making the environment a perfect storm for Judges. Management shared why the current environment makes closing acquisitions challenging:

The context of that question, if it’s intended in a long-term view, I think yes, we are still finding good businesses to buy. We don’t see it as something which is getting harder in a sort of sustained or systemic way. I think what we would highlight is the current environment is challenging. We are looking to acquire high quality businesses with owners who wish to sell, but they may not wish to sell off the back of a poor year if there’s been a poor year, or they may have a particular number in mind, and that number in mind may imply a higher multiple or a higher valuation if they’re not performing at their best at the moment. What we’re tending to find is that sellers are patient and we need to be patient as well. While there may be opportunities to acquire lower quality businesses, that’s not our strategy.

This makes sense and I don’t view it as an excuse considering that it’s not the first time management has shared this with shareholders. The good news on the acquisition front (if any) is that Judges has significant dry powder to pounce on acquisitions when sellers are willing to sell. Gearing (i.e., leverage) calculated as net debt/adjusted EBITDA was 1.5x at the end of the year and the company can take it up to 3x before violating any covenants.

So, what’s the dry powder? Assuming that the company wants to go to 2.5x leverage (3x would be a bit too much) and that Adjusted EBITDA will most likely fall next year by around 10-15% to 26 million pounds, Judges could potentially borrow an additional 26 million pound to fund acquisitions should it need to. To this we must add the cash that the business expects to generate next year (let’s say 25 million pounds), meaning that total dry powder is likely going to be close to 50 million pounds. 50 million pounds deployed at an average EBIT of 5x means that Judges can potentially acquire 10 million in EBIT with its current dry powder (for context, current EBIT is lower than 30 million).

So, if we add everything up we can conclude that the 2026 guide includes…

No improvement in US funding

No Geotek contract (one of those 4 years in which management doesn’t believe there will be one)

Nothing assumed in terms of acquisitions

While Judges’ stock was negatively “exposed” to these three “events” a year ago, I believe it’s now positively “exposed.” What I mean by this is that the company is trading at 19x 2026 EPS, but that this EPS seems to have a very positive skew to good news. I guess we’ll find out soon enough.

It also seems obvious that the new management team wants to increase the focus on the operations of the business, not just M&A. Several things point to this being the case: R&D expenses are increasing, management claimed that they’ve made several changes to the MDs (managing directors) of their businesses, and they also hinted at sharing innovation-related KPIs in the future. I believe David Cicurel correctly understood that Judges has now reached a size where operational excellence matters (more so considering how lumpy acquisitions can be) and that he is better off focusing on M&A and leaving operations to others (former Halma executives).

The last point I wanted to discuss today is the conflict in the Middle East. Direct exposure to the Middle East stands at 2%, although we already know how uncertainty can weigh on Capex spending. Now, this said, management believes that persistently high oil prices can even be beneficial for the business, something which should flow through Coring (as customers look for other hydrocarbon sources) and through the businesses that are exposed to offshore wind farms:

Our sense of the high oil prices or correlation with the oil price or a correlation of the realization of how sensitive the world is to certain restrictions. For example, the Strait of Hormuz and who has control over that would, you know, beg the question, well, is that gonna accelerate countries who are currently rely on that to take a look at alternative arrangements, whether that means a faster transition to wind power, for example, or other green energy technologies, or whether that means investigating alternative hydrocarbons.

Yeah, it is the case that the methane hydrates that form the basis of these coring expeditions are vast resources of alternative hydrocarbons. You know, it’s rather speculative. We just don’t know, and these things would take many years to develop. It could be that if the oil price stays at a sustained high, and if the volatility in that particular region remains the case, you know, that could be a long-term driver for that.

So, all in all, weak current earnings as expected, but things seem to be starting to line up in Judges’ favor. The company has remained very cash generative throughout the “perfect storm” and it does seem like 2026 will be the bottom of the cycle (still TBD). With the company trading at 19x trough EPS and the thesis intact, I view the shares as attractive.

Have a great day,

Leandro

Really terrific piece. I've also been looking and reading about Judges and the developing university situation. I saw the Congressional appropriators move earlier in the year and thought the firm might be a beneficiary, but I hadn't fully appreciated the Geotek reversal. Thanks for writing it!

Great note Leandro.

As it happens I published on Judges 7 minutes after you!

https://charliehuggins.substack.com/p/judges-scientific-full-year-results?utm_source=share&utm_medium=android&r=g8woi