Earnings better-than-feared and Management’s PSUs

Shift4's Q1 2026

Shift4 reported better-than-feared Q1 earnings yesterday. I must say that my expectations coming into earnings were not great, for two main reasons:

Payment peers were not reporting great earnings and were getting smoked by the market

Global Blue was going to surely be impacted by the conflict in the Middle East as its business depends on tourist flows

Both of these remain true even after Shift4’s earnings, but the company still managed to deliver good earnings. Most KPIs were in-line or ahead of management’s expectations. The stock (surprisingly enough) reacted positively, although it’s still trading at a similar level than it was post-Q42025 earnings:

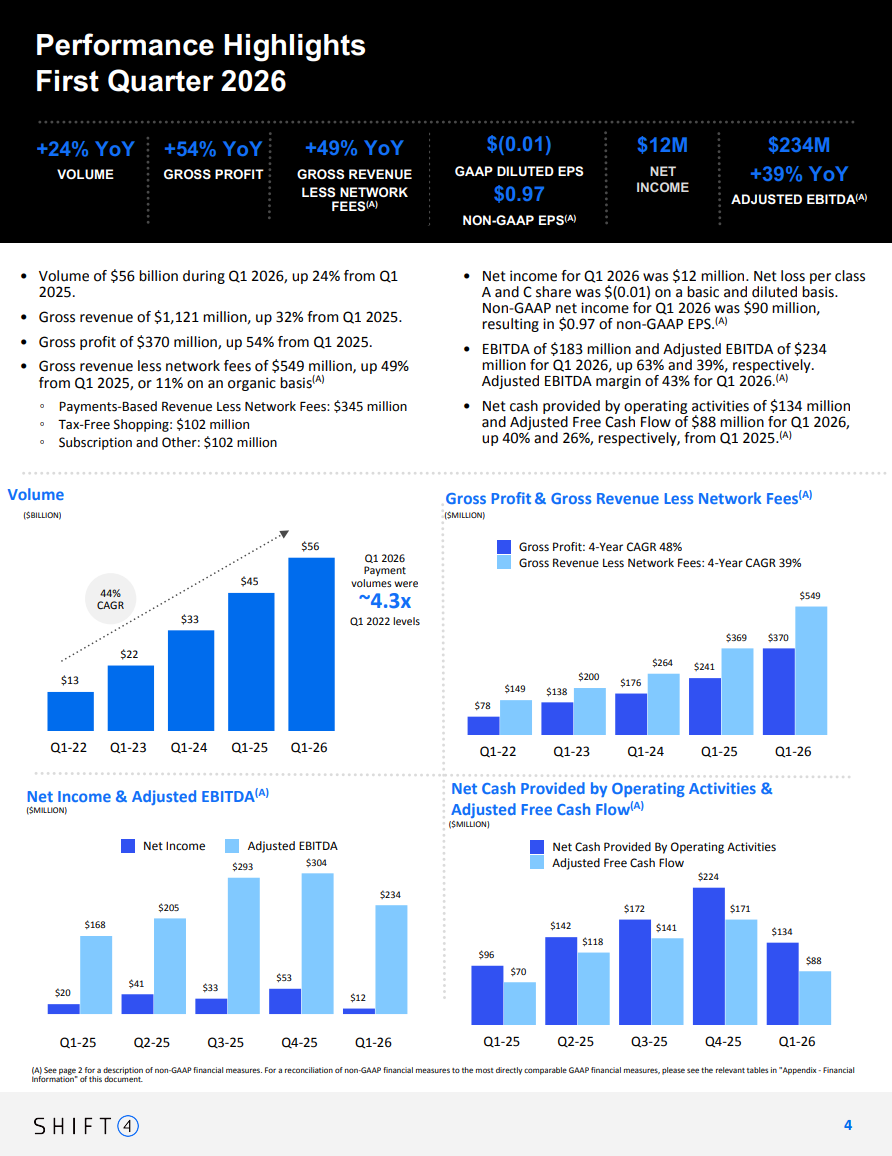

Let’s begin by sharing the first page of the shareholder letter as a summary of the quarter:

Pretty healthy numbers all around, but it’s not these where I want to focus on today. The first KPI (not highlighted in the slide above) that I want to focus on is organic growth. Two positive things happened here. First, Shift4 is going to start calling it by its name and seems like it will start disclosing it recurringly. This is great news because it’s what the market wanted as there has been historical skepticism about Shift4’s ability to grow organically.

The second good news concerning organic growth was the number per se: +11%. Despite the Global Blue softness and despite a 400 bps drag from the “grandfathering” of legacy revenue sources, Shift4 managed to grow double digits organically. Trends were even healthier in the America’s region (in which the reported number is basically a proxy of organic growth): +15%. This is interesting considering that it’s Shift4’s most mature geography, but I believe this is precisely what makes Shift4’s story appealing:

We can grow substantially without finding a new customer and we can drive meaningful margin and free cash flow improvement by simply continuing to do what we do well, which is integrate our businesses and delete the parts.

There’s still a lot of cross-selling to be done across Shift4’s customer base, and even though it’s true that this organic opportunity is somewhat reliant on M&A (at least its durability), one also has to understand that it’s all a tradeoff. What the market understands as pure organic growth (i.e., organic growth not reliant on M&A) would arguably be higher if Shift4 redirected the funds it invests in M&A into organic initiatives. Management simply doesn’t believe this is the best use of cash.

The other focus of the release was Global Blue. As I have discussed in several recent NOTW, the conflict in Iran promised to be a pretty significant headwind for Tax Free Shopping. Well, TFS actually came in at +4% YoY despite this impact (only slightly below the MSD growth guided for the year). The impact promises to be higher in Q2, but the conclusion here is…yes, Global Blue came in weaker, but the conservative guide and the outperformance in other segments was enough to help maintain the yearly guide. Good news.

Also note that Global Blue gives Shift4 something unique: the Shift4 One payment terminal. This product combines payments, DCC, and Tax Free Shopping and management expects it to be critical in converting Global Blue’s customer base to payments:

This is the product that will help us unlock the meaningful revenue synergies within the SMB install base of luxury retailers that are already tax-free shopping customer of Shift4.

This product is already live in 7 countries and will be in 15 by the end of the year. What’s interesting is that management told investors not to expect any meaningful revenue synergies from Global Blue in FY 2026 (if I recall correctly) but they seem to be executing pretty fast. Early customer wins were companies like Breitling and Swatch, and it also seems that features such as the ones that Shift4 One enables will probably be very relevant for the World Cup this summer.

Management also said something interesting regarding margins:

We do see a path back to 50% margins as we sufficiently scale our international operations, but will balance the growth opportunity appropriately.

The company has been investing aggressively in international expansion (which is scaling nicely and showing good prospects) but believes margin expansion is in the books once these investments start to show returns. The 50% Adjusted EBITDA margin objective is not dissimilar to what the company achieved in 2025 (48.9%), so what they are basically saying here is that the Adjusted EBITDA margin delivered in Q1 2026 of 43% is probably not representative of what can be achieved over the long term. The admission that Adjusted EBITDA margins might expand 110 basis points is good, but I don’t think it’s game changing considering the company’s valuation and the fact that it’s growing organically double digits (i.e., it’s not critical but good news nonetheless).

Another historical bear case for Shift4 (and payment companies in general) were spreads. Some people seem to believe that payments are unequivocally a race to the bottom, but Shift4 continues to experience stable spreads. I know this might be a total narrative violation, but Shift4’s spreads have been stable for a pretty long while despite the fast growth. Management believes that the Street doesn’t really understand competitive dynamics inside of Shift4’s industries and used the restaurant example (the most competitive industry) to illustrate their point:

There is not a lot of changing of pole position with regard to the competitors we see and admire in our markets and how we face off compared to them. Our restaurant point of sale product is growing location counts 40% YoY. I think it probably surprises the street. It does not surprise us.

While the market remains skeptical about the Shift4 story, management is doing what they have to do: repurchasing shares:

In Q1, we repurchased 5.5 million shares, resulting in a cumulative $600 million of executing against the $1 billion share repurchase authorization announced 2 quarters ago.

The topic of buybacks is interesting, more so when viewed in the context of the newly announced compensation plan. Shift4 published its Proxy Statement a couple of weeks ago. In it, they shared what the PSUs (Performance Share Units) would be based on. I conducted an exercise to understand what needs to happen to the “organic” business so that management achieves 100% vesting of the PSUs. The goal here is pretty much to understand whether the objective tough to achieve or not (i.e., whether management is being “handed” these PSUs).