Does the market get noisier in December? (+ some clarifications on Shift4's TRA liability) (NOTW#73)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

The indices were mixed this week as the AI-trade somewhat “recovered.” This time of the year is typically a slower one due to holidays…but that’s not the only reason. In the brief market commentary, I discuss why markets might get noisier toward the end of the year (although it’s fair to say that they are noisy all year round!).

In the company-specific section, I’ll discuss something that people are likely misunderstanding when it comes to Jared’s departure from Shift4 and how that impacts the TRA liability. The company-specific section typically contains pretty relevant news and research pieces on companies I own but that might not merit an individual article. For example, I was writing about Nintendo for this NOTW, but decided to write an individual article when I saw how long it was becoming (will probably publish it on Monday).

Without further ado, let’s get on with it.

Articles/Webinars of the week

I did not publish any articles this week but held the first Best Anchor Stocks webinar.

In the webinar, I discussed…

How I calculate ROIC/ROIIC, the advantages and limitations of these variables, and how to interpret them

The Reuters article on ASML that claimed that China already has an EUV prototype

Q&A (there were some great questions related to AI, portfolio management, returns…)

If you are a paid subscriber you can access the recording, the presentation, and the ROIC model here. One subscriber also suggested doing webinars on specific companies that I’ve profiled, and I’m considering that as well.

Market Overview

The indices had a mixed week. The Nasdaq was up 1% whereas the S&P 500 was flat:

I don’t think we should never read too much into what happens in any given week, month, or semester, but less so during December. Two things occur in December that probably make market movements even noisier than they usually are. The first one is that trading volume tends to go down due to the Holiday season. Each year is a different beast, but barring significant events in December, it tends to be the weakest volume month of the entire year (more so as we approach Christmas).

The second thing to consider is that there’s typically significant tax loss harvesting as we get to year end. Investors/traders/speculators close some losing positions, with two objectives in mind. First, to take advantage of the tax break that comes from selling a losing position, and secondly, to somewhat improve the look of the portfolio as Q4 and the year get to an end (this is called window dressing). Note that, in many cases, investors might buy their shares again the following year. This all seems logical, but is there any evidence that it really takes place? Let’s see.

The first one is probably an anecdotal observation, but stocks that are down for the year tend to remain weak (or can be even weaker) as the year gets to an end. In some cases, these stocks can go down without receiving any relevant news for months. The second reason, also anecdotal, is that one can see a lot of people actually saying that they are selling positions to tax loss harvest (don’t think this is as applicable to funds where window dressing might be more of a consideration). There are several studies that show that trading volumes for losing positions are “abnormally high in December and abnormally low in January.”

The third (and final) reason can be encapsulated in the January effect. The January effect states that January returns tend to be higher than those of other months of the year. More specifically, some studies “demonstrate” (always worth taking these with a healthy dose of skepticism) that the stocks of small and mid-cap stocks tend to do significantly better in January if they did poorly the year before (somewhat supporting the tax-loss selling hypothesis).

I highly doubt that everything I’ve just discussed applies to a great extent to large and mega caps, but it might definitely be true for smaller companies or those that have low float. Note that the “deadliest” combination is: small cap/float and bad performance during the year. The low float/volume means that you don’t need much selling pressure to see large swings in the stock price, and the bad performance surely makes it a tax-loss harvesting candidate. Not ideal but not really relevant for anyone who invests long-term.

The industry map was mixed this week:

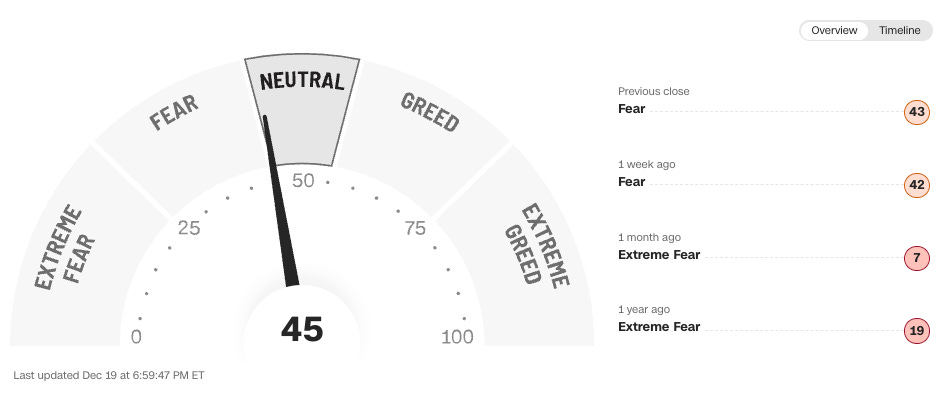

The fear and greed index improved slightly but remained in fear territory:

What I bought this week

This week I added primarily to two companies which I believe have gotten swept into narratives that don’t make sense. Next week I’ll probably add significantly to a position that is also swept into a narrative and that I believe is pretty cheap. It currently makes up 5% of my portfolio, it’s a newish addition, and it has become even cheaper due to exchange rates.

This is what I bought: