Contextualizing the conservativeness

Nintendo’s FY 2026

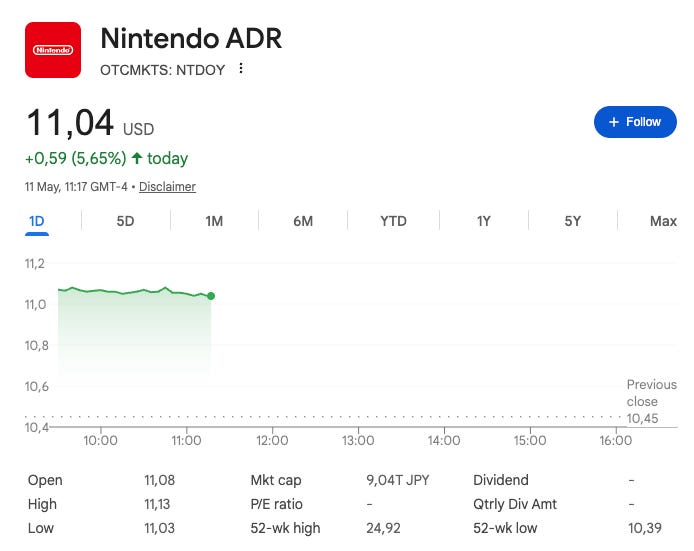

Nintendo reported FY 2026 earnings on Friday last week, and the market did not particularly like these. The US ADR (NTDOY) dropped almost 12% but, in an incredible twist of fate that I did not expect, the shares dropped considerably less in Japan on Monday (-9%) considering that they had been up 4% on Friday before the earnings. For the first time in a long while, the Japanese investors saved the day and the ADR rebounded strongly on Monday:

Now, even after this minor upswing, Nintendo remains down 35% YTD and 55% off ATHs.

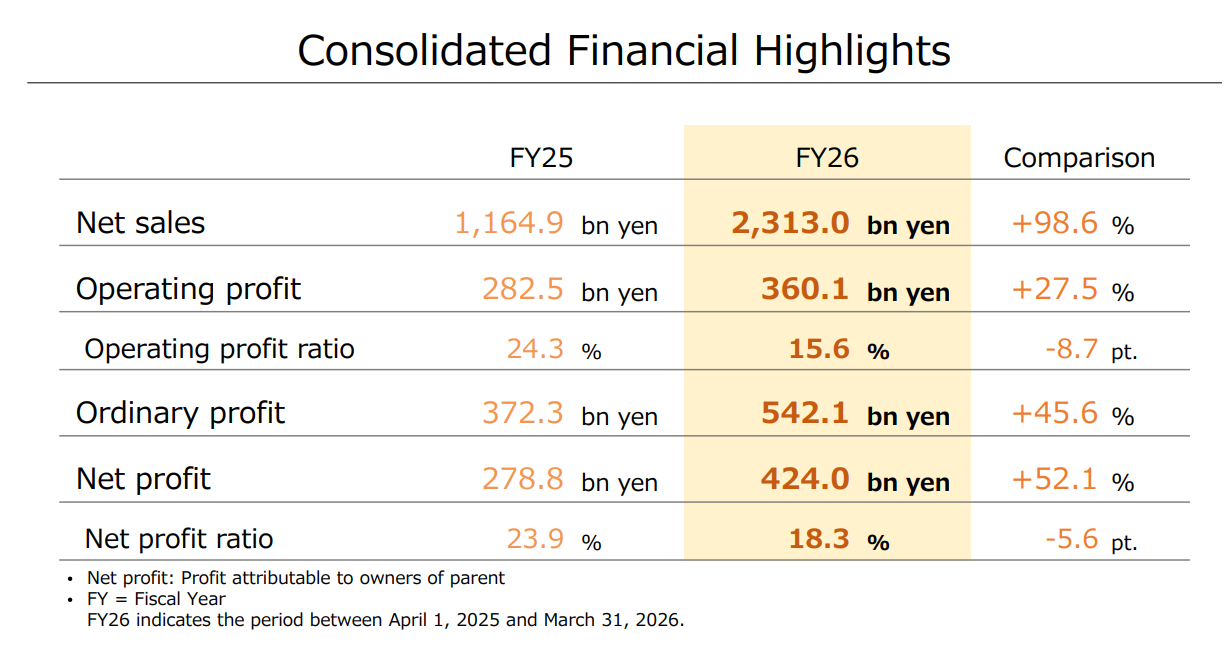

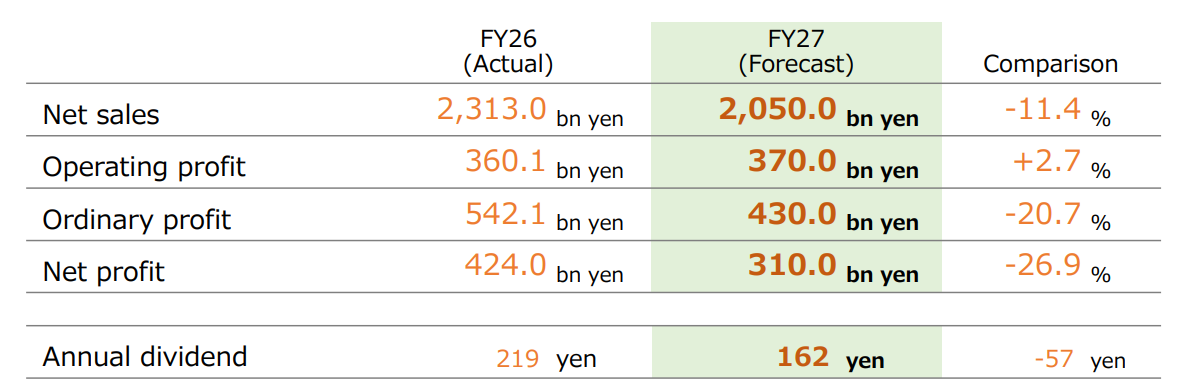

So, what earnings did Nintendo report? I believe they were a tale of two halves and we must differentiate between FY 2026 earnings and the FY 2027 guide. These two were night and day but are also somewhat related (I’ll explain why later but I’ll give you a clue: “anchoring”). Nintendo reported very good FY 2026 earnings, with the first “year” of the SW2 cycle significantly beating the most optimistic of expectations. Sales grew almost triple digits and operating profit rose 27.5%:

Nothing here should surprise investors directionally. During the first year of a console cycle, it’s normal to see sales grow significantly faster than operating profit as margins compress due to an elevated hardware proportion (which carries lower margins).

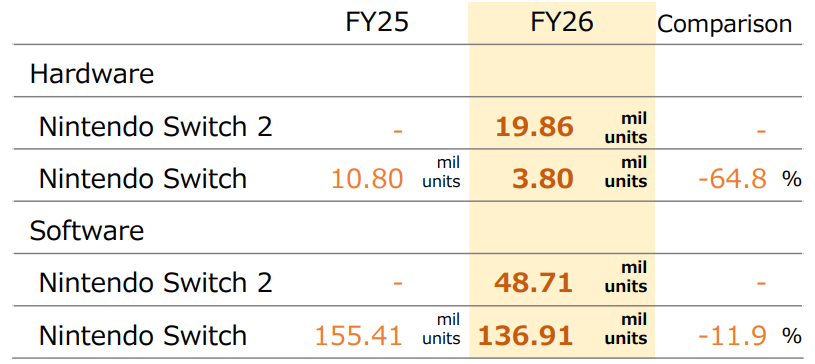

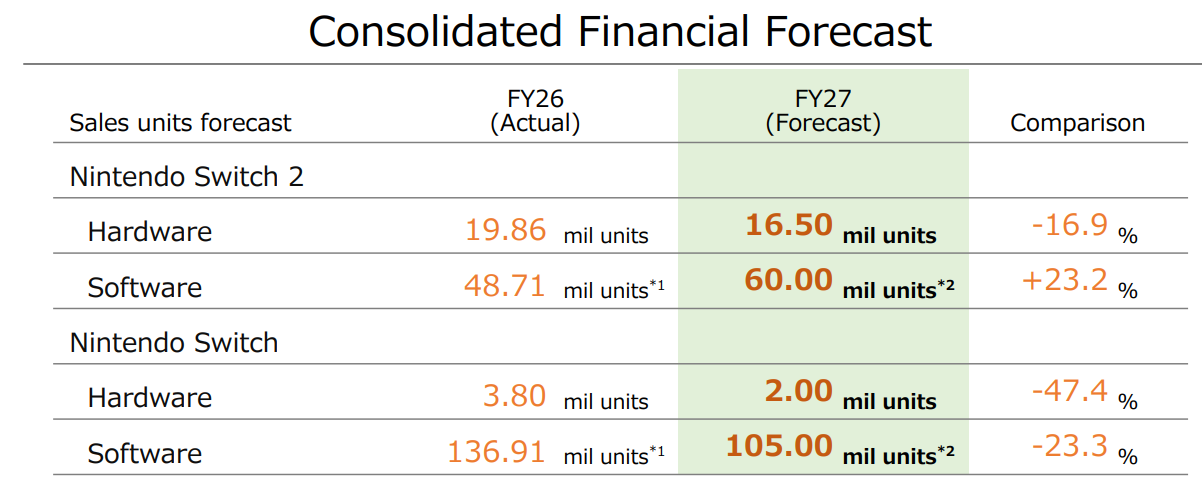

These results were possible thanks to the spectacular debut of the SW2. Nintendo sold 19.9 million SW2 units and 3.8 million SW1 units (down 65%) in FY 2026. Software also did well, selling 48.71 million units in the SW2 and 137 million units in the SW1:

People sometimes forget that the SW1 business also belongs to Nintendo and that it’s still a thriving business; 3.8 million hardware units sold and 137 million software units sold in an eighth year of a lifecycle is a feat not many have achieved before.

Anyways, before discussing the guide in more detail, I believe we should use Nintendo’s initial FY 2026 forecast as the initial sign of conservativeness. Nintendo guided for the following financial objectives at the beginning of the year:

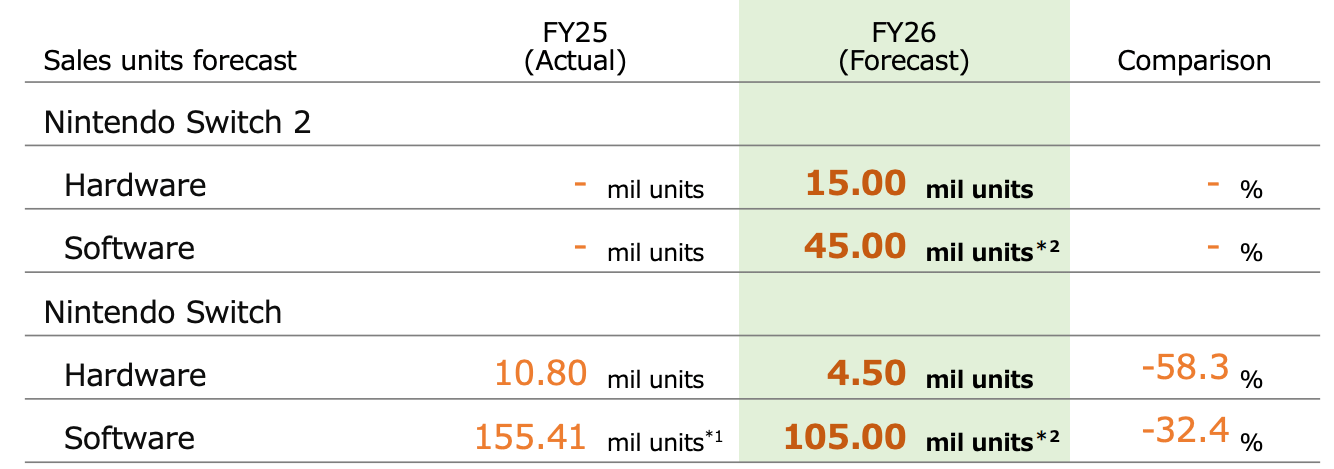

If we compare these to what Nintendo ended up achieving, we can see that the company ended the year 22% ahead of its initial revenue guide and 12.5% ahead of its operating profit guide (and this is despite increased tariff costs). Things don’t change much when looking at the hardware/software guide. Nintendo began the year with the following expectations:

The company delivered SW2 sales 32% ahead of its expectations and software units sold 8% ahead of their expectations. The company also incredibly sandbagged software sales for the SW1, which ended up being 30% ahead of their expectations. I heard someone say that if someone using the SW2 buys a SW1 game, it’s counted as a SW1 sale (which might explain the divergence), but adding both platforms together what we can conclude is that Nintendo expected 19.5 million hardware units sold and 150 million software units sold at the beginning of the year (SW1 + SW2) but ended up delivering 23.66 million hardware units (21% beat) and 185.62 million software units (24% beat).

Nintendo’s ADR was at $20 when it set its FY 2026 guide and later went to $24. It’s at $11 today after having blown through those estimates, although it’s true that there are other problems today that are impacting forward-looking guidance (more on this later). Nevertheless, the sheer outperformance that Nintendo managed on its FY 2026 targets should help us contextualize the recent guide.

The market’s focus: the guide

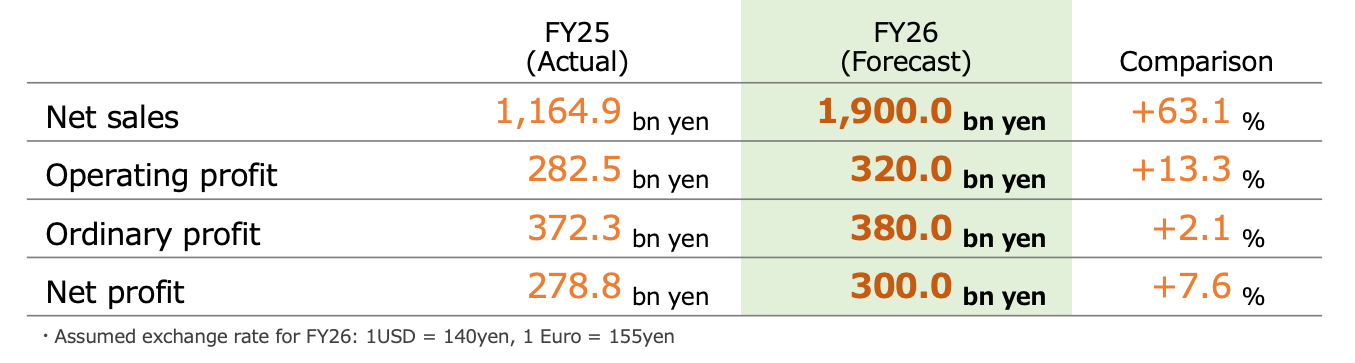

It seems like Nintendo’s expectations took many by surprise (myself included). This is the company’s financial guide for FY 2027:

And this is the guide in terms of hardware/software:

I believe that the exercise I did above should’ve demonstrated that Nintendo is typically conservative with its guide, but the guide was “soft” even for Nintendo’s sandbagging standards. Many things are required to fully understand the guide, let’s go over these.

First, Nintendo is expecting a 100 billion yen impact in FY 2027 from tariffs and component pricing (i.e., higher memory prices). Should this impact be absent, operating profit expectations would’ve been around 470 billion yen for 30% YoY growth. Imho, and despite this impact, this financial guide lets the Nintendo thesis shine through: it’s software that eventually drives the margins as the system scales.

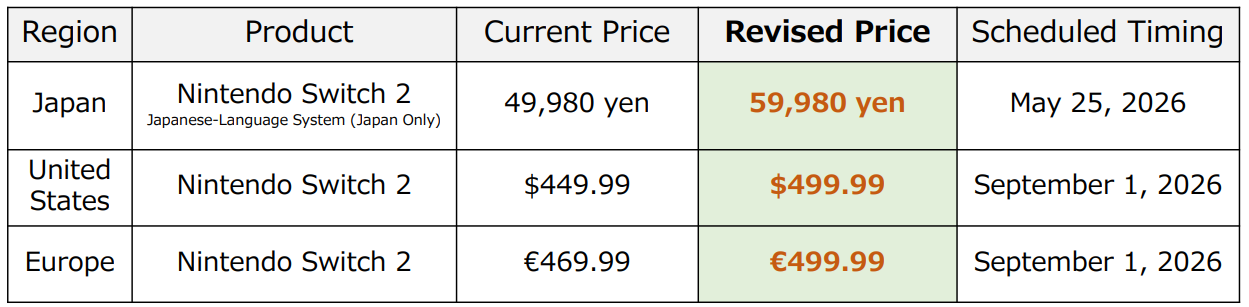

Now, there’s no denying that timing has been very unfortunate and Nintendo has to live with higher memory chip costs. Management now believes that memory pricing is a longer-term problem than previously anticipated, so they decided to raise prices:

There’s a lot to discuss about these price increases. The first interesting aspect is the timing. Even though prices are going up almost “automatically” in Japan (where the SW2 was cheaper to start with), Nintendo has decided to wait until September to raise prices in Europe/US. Before reading the Q&A, I speculated that this was being done because Nintendo wants to announce a strong software line-up for the holiday season that would justify higher prices. Management later “confirmed” in the Q&A that there are unannounced games for the second half of the year (not a surprise to anyone tbh). He also told consumers/investors that they’ll release software to justify the higher price in what I would consider a “bold” claim for Nintendo’s standards.

The second interesting aspect of the price increases is what it can cause in terms of pull forward of demand. SW2 prices are increasing relatively soon in Japan and the SW2 (at the current price) is being sold out across many stores. Hopefully, Nintendo has enough inventory to satisfy a pull forward that might also come in Europe/US.

I honestly don’t think that these price increases change the thesis much, but I believe it’s also evident that management is unsure how they will impact demand and therefore likely took a negative impact into account in the guide. Nintendo is not known for lowering prices, but it’s also not know for raising prices soon after launch, so we could consider this uncharted territory.

What’s interesting is that, if management believes that it would make the SW2 less “affordable,” this should be reflected in higher SW1 sales (which doesn’t seem to be the case either in the guide). Anyways, the bottom line is that Nintendo is now planning for a world where memory prices continue to go up over the long term and that’s good news because there’s now upside to whatever happens going forward:

We expect prices to continue rising going forward, and from the current fiscal year onward we anticipate this will become a gradually increasing headwind to hardware margins.

The second thing I’d like to comment on is that Nintendo’s management seems fixated on the SW1 rollout as a proxy for the SW2 (i.e., it seems they are using the SW1 launch as a benchmark). Both on the prepared notes and the Q&A, management talked about the SW1 cycle when contextualizing the SW2 guide.

For the current fiscal year, our initial forecast of 16.5 million units reflects current sales momentum as well as the historical second-year sales levels of our dedicated game consoles. As noted in the financial results presentation materials, the pace of Nintendo Switch 2 adoption is tracking ahead of Nintendo Switch and we have no particular concerns about that momentum at this time.

It seems that they believe that the SW2’s launch year has been “too good to be true” and that, as they are in uncharted territory, they’ve decided to anchor in the velocity of the SW1 cycle (can’t blame them). Now, this may or may not be true, but I find it unlikely that SW2 sales will be down in FY 2027 IF (big IF) there’s a strong 1P system seller in the year. A Mario 3D game makes a lot of sense considering that…

It’s Mario’s 40th anniversary

It would come after the Mario movie and therefore would benefit from the “Halo”

If I had to guess I’d say that a Mario 3D game is highly likely, which makes the guide look even more conservative, why? Because a Mario 3D game is the kind of system seller that moves the needle. Let’s review some former 3D Mario releases:

Super Mario Odyssey, launched in October 2017 and sold 29 million units. Nintendo took advantage of its Mario 3D franchise to push the sales of the SW1 early on because the company could not afford a flop after the Wii U. The environment today is pretty different because Nintendo knew that the SW2 would not be a flop and therefore could save the system sellers for years 2/3

Super Mario 3D World + Bowser’s Fury, launched in 2021 and sold 13.47 million units

Management is also very aware that it’s these 1P releases that will allow them to grow the hardware business. During the call management claimed that after a weaker-than-expected holiday season outside of Japan, things started to trend in the right direction thanks to Pokemon Pokopia and Tomodachi Life. It’s the software that sells the hardware and we’ve had little exclusives this year (which has incredibly not weighed on hardware sales)...

The contribution of Pokemon Pokopia to hardware sales reaffirmed our conviction that having software customer genuinely want to play is a critical driver of migration to Nintendo Switch 2.

…but we know for a fact that more things are coming in H2 2027…

For the second half of the current fiscal year, we have new titles in preparation beyond those already announced and we will share details at the appropriate time.

…which management is unlikely to have taken into account when setting the guide this early on, especially since they typically sandbag software sales despite them being Nintendo’s bread and butter. The quality of Nintendo’s IP became strikingly evident in the earnings release with the great successes of Pokopia, Tomodachi Life, and Pokemon Fire and Leaf. To this we must add potential optionality from 3P system sellers…is GTA VI coming to the SW2? Some rumours point out it will, but we still don’t know.

All in all, even though the guidance was soft even for Nintendo’s standards and the fact that the memory crunch has come at a very unfortunate time (when hardware has just started scaling), I believe these are “solvable” problems. The guide seems pretty conservative and it’s evident that it’s set based on what the SW1 did, whereas the memory crunch will not last forever (regardless of what people claim). This means that Nintendo might be in for some short to medium term “pain” (which seems to have been taken into account in the guide) but that the thesis remains alive and well. I am considering adding to my position at current levels.

Have a great day,

Leandro