Constructive but not there yet

Danaher's Q1

You can read this article entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

I published yesterday an article on a relatively unknown business: Rosebank Industries. You can read that here:

Join today:

Danaher reported decent Q1 earnings yesterday. There was nothing too surprising or worrying in them, but there were two good news:

Management (very) slightly raised the 2026 EPS guide from a midpoint of $8.43 to $8.45 (I know, it’s honestly not very meaningful)

Management confirmed that Q1 trends are encouraging and openly shared what needs to happen for the company to end up in the high end of the core revenue growth guide for the year (more on this later)

The reality is that Danaher has faced several headwinds that haven’t allowed the company to grow at an acceptable pace for a while. The company saw a huge pull forward (both in consumables and equipment) during the pandemic which ended up resulting in a bust once customers began to draw down their inventory. Besides the destocking, the company also faced subdued biotech funding. When these headwinds finally began to transform into tailwinds, the company experienced two additional headwinds:

The VBP (Volume Based Procurement) situation in China (primarily impacting the diagnostic segment)

Lower Capex spending by customers driven by geopolitical uncertainty. This impacted equipment revenue while consumable orders improved post-destocking. Management, however, believes this will transform into a headwind in due time:

At the same time, equipment investment has been relatively muted, which we believe created a growing need for incremental capacity in the coming years. We’re encouraged by improved trends in bioprocessing equipment and believe we are in the early stage of a multi-year investment cycle.

There was also, btw, “good” (or at a minimum, “encouraging” news) for Judges Scientific:

While demand at academic research customers remained muted in the quarter, we saw early signs of momentum building in our order book.

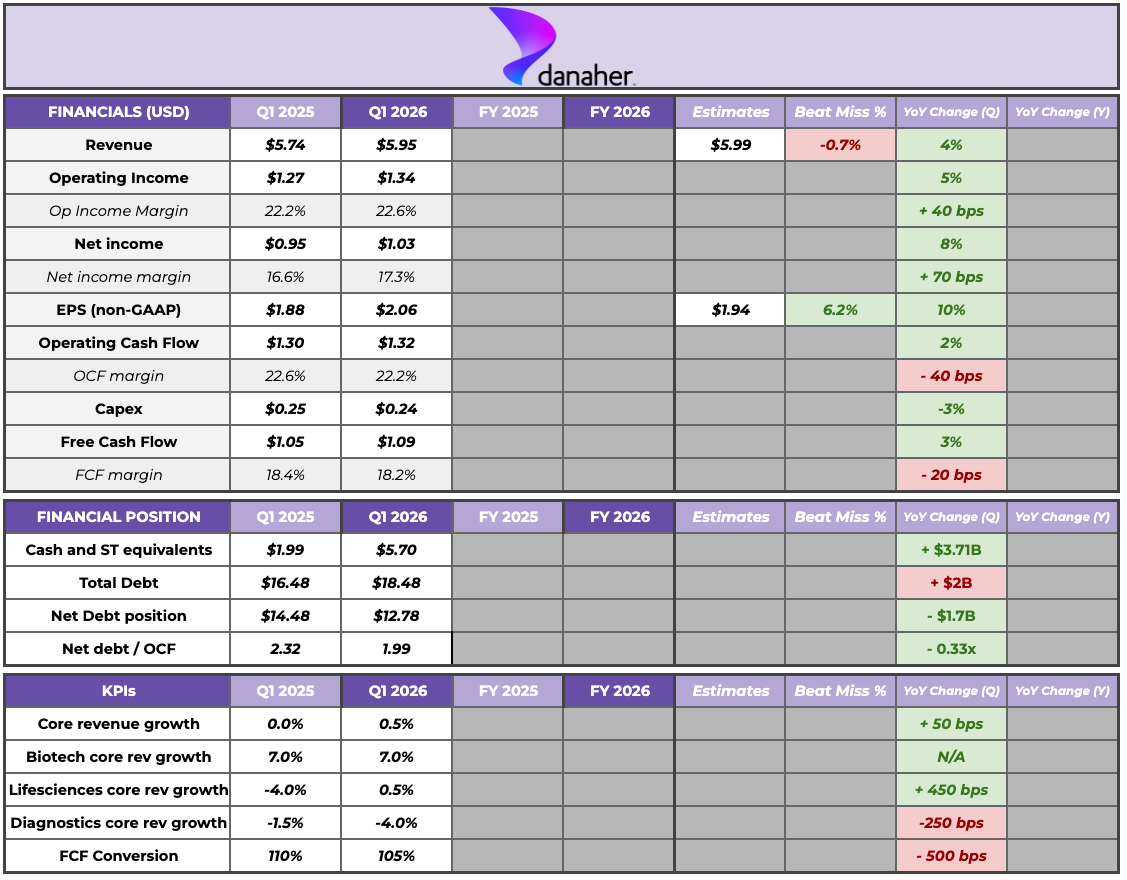

So, let’s take a quick look at the results. Here’s the summary table:

The main things I would highlight from this table is that revenue growth remains “meh” but that earnings are growing significantly faster than the top line, driven by cost containment measures and DBS. Management believes that EPS can grow HSD/LDD this year even while remaining at the low-end of the core revenue growth guide (+3% YoY). One can only ask themselves what would happen to EPS growth if Danaher manages to be at the high-end of the guide (+6% YoY). Let’s not ignore that operating profit margins (adjusted) rose 60 bps in a no-growth quarter.

So the question here should be: what takes us to the high end of the core revenue guide? Management explained that Q1 was off to an encouraging start in terms of trends, something that would suggest that growth is trending ahead of the low end:

Across the portfolio, trends in many of our end markets were modestly better than our expectations entering the year.

Biotechnology and Life Sciences strength compensated for the lower-than-expected respiratory season (i.e., diagnostics came in below expectations with respiratory revenue down 25% YoY). The weaker respiratory season made management lower their expected respiratory revenue from $1.8 billion to $1.6 - $1.7 billion. They, however, expect the other segments to fully offset this drop.

Management also shared what caused Biotechnology and LifeSciences to perform ahead of expectations. There was a common driver for both: China. Equipment is also getting better and showing encouraging signs in Biotechnology, but it’s not showing in the numbers yet:

Equipment declined modestly in Q1, but we were encouraged to see orders growth of more than 30%, marking the first quarter of year-over-year equipment order growth in nearly two years.

Management is not assuming these orders convert to revenue over the short term (i.e., it theoretically doesn’t impact the 2026 guide), but they do believe it’s great news for the post-2026 period.

Most analyst questions were focused on 2026 numbers (surprise!): will Danaher be able to be at the top end of its 3%-6% growth guide? Management did not provide an answer but did share what needs to happen (albeit not quantifying anything and simply providing directional comments). It comes down to 5 things:

Further improvement in life sciences: management admitted being encouraged by Q1 trends but they need these to continue throughout the rest of the year

China: even though China was off to a good start in Q1, management believes the high end of the guide requires additional acceleration

Biotech funding: management wants to see improved funding convert quicker into orders

Bioprocessing: requires higher than HSD growth (which seems possible if equipment improves and orders start converting to revenue)

Respiratory season: after a slow start to the season, they will probably need an “above normal” Q4 respiratory season

So, lots of things need to happen for Danaher to grow its top line 6% this year, but with #1, #2 and #3 trending better than what was expected at the start of the year, I’d say that Danaher should end the year above the low end of the guide.

In January, we said there are three things that really needed to happen to support the ramp throughout the year. All three of those things played out as we expected, or actually even a touch better in Q1.

This is important because 3% core revenue growth is where Wall Street is currently anchored. Anything above the low end of the core revenue growth guide should translate to LDD EPS growth, which is not exceptional considering where Danaher comes from but I’d define it as constructive considering the ongoing headwinds. This is arguably a feature (not a bug) of diversified businesses: it’s tough for everything to work at the same time and it sucks when one segment’s poor performance is obfuscating the good performance of the others, but that can also become an advantage when things are not going great (and if not one simply has to look at the charts of pure-play bioprocessing businesses through the destocking).

Management also talked about other relevant long-term topics. The first one was the implications of AI in the business (I wrote an article about why I consider healthcare to be positively skewed to AI here):

We also believe the emerging opportunity in AI will further accelerate the pharma development and commercialization flywheel. This improves success rates, lowers development costs and drives increased demand. This, in turn, is expected to drive incremental demand for our life sciences solutions, as well as in bioprocessing as commercial drug production expands.

The average yield in the drug development pipeline today is just above 10%. There is an enormous opportunity here to improve the yield of the pipeline.

The second relevant topic was M&A. Danaher recently announced its intention to acquire Masimo (I wrote a detailed article on the acquisition here) and I was surprised to see management not rule out additional M&A over the short term:

From a balance sheet perspective, post-close of Masimo, we will go to about two and a half times net debt to EBITDA. Given our strong free cash flow of $5 billion+ per year, as well as EBITDA generation, this leverage will come down fairly quickly. It gives us the ability to remain active on the M&A front, even in the near term.

All in all, not much has changed for Danaher in Q1. Things are getting constructive to end above the high-end of the guide, but the market remains in “show me” mode.

Have a great day,

Leandro