Constellation's Q2 and Valuation

Is the company expensive?

Hi reader,

Constellation Software, my largest position (by far), reported earnings on Friday. These were good, as they tend to be. There’s some volatility in organic growth, which has gotten some people worried, but besides this volatility needing context, I believe there was much more to like in the earnings than not. This quarter also provided a good representation of why looking at the net income figures for Constellation is always extremely misleading. Cash flows are what any investor should focus on when analyzing any business, but this stands even more true for a company like Constellation.

Recall that Constellation does not hold earnings calls, so if you want an update on the qualitative highlights you have to watch/read the latest Annual General Meeting. This article is shared for free, with the only exception of the section on valuation, which is reserved for paid subscribers. If you want to have access to all the content, don’t hesitate to subscribe:

Without further ado, let’s get on with the quarter.

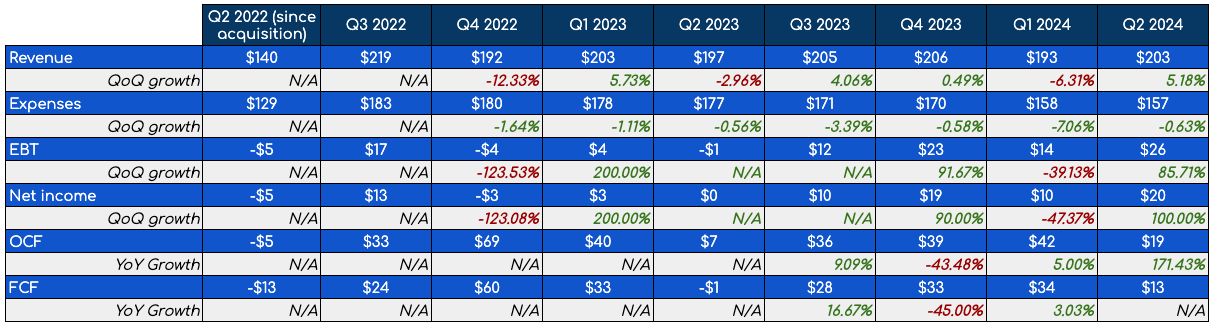

The numbers

Constellation reported another outstanding quarter, growing its top line by 21% year over year. As you can see below, net income grew a whopping 71% year over year, but this growth needs context as it was caused by several non-operating expenses and the absence of the Lumine redeemable preferred securities expense (discussed in more detail later):

The company did not enjoy operating margin expansion this quarter, but it did for the first six months of the year:

I don’t think there’s much to worry about here because a logical conclusion would be that, being an acquisitive company that doesn’t typically buy the best businesses in the world, we shouldn’t expect Constellation’s current margins to be optimized. In short, if Constellation stopped acquiring companies today and started to streamline its costs, we would probably see significantly higher margins than those we see today. Of course, that would probably not be the best outcome for investors as it would somewhat signal that the acquisition runway is over and growth would fall significantly.

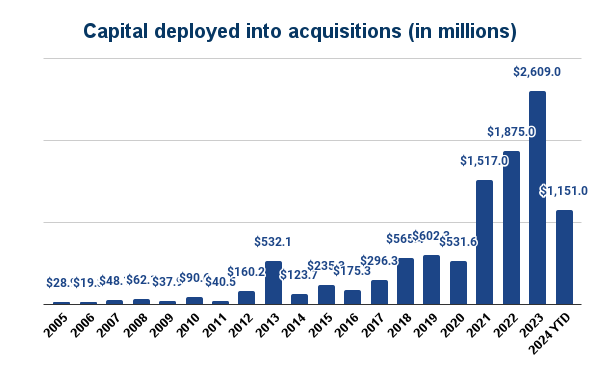

It remains impressive how Constellation continues to grow and deploy capital as it scales. Quarterly revenue growth decelerated somewhat sequentially but still remained above the 20% mark. Being an acquisitive company, it’s normal to see some sort of lumpiness here. I think that overlaying capital deployment and revenue growth allows us to see a clear illustration of what I’m talking about. Large capital deployments tend to be followed (with a lag) by an acceleration of revenue:

Constellation is nearing the $10 billion revenue run rate (currently at $9.3 billion), and it’s still growing at 20% rates. This is pretty rare, but instead of me telling you this, let’s use Finchat to understand how many US/Canada listed companies satisfy three conditions that Constellation satisfies:

Revenue 3-year CAGR above 25%

Revenue run rate above $8 billion

Free Cash Flow margin above 20%

Finchat’s screener shows 6 results out of a universe of hundreds of companies:

I'm bringing this small exercise to underscore how impressive it is to grow at this pace at this scale. Constellation is a unique company that has deferred the forces of capitalism and the law of large numbers for quite some time. The law of large numbers has been cited as a bear case for large companies for quite a while, but it’s useless without context. It’s not so much about how large a company gets but how large it gets compared to its target market. Constellation’s runway is still significant because the VMS is constantly growing.

Digging deeper into revenue

As you might already know, Constellation has two sources of revenue growth: acquisitions and organic growth. Acquisitions were again responsible for the bulk of the company’s growth, but organic growth remained somewhat resilient:

Organic growth started to decelerate as soon as Constellation started to face tougher comps (Q1). This was to be expected, considering that the company probably took advantage of inflation to increase prices considerably in 2023. With inflation now subsiding, this is arguably a much tougher conversation with customers. This is something I flagged in my Q1 article, which was confirmed by Mark Leonard during the AGM.

The good news could again be found in management’s preferred revenue source: maintenance and recurring revenue. Despite overall organic growth trending somewhat lower due to tougher comps, maintenance and recurring organic revenue growth has remained more resilient:

Constellation has grown its preferred revenue source above 5% for 13 consecutive quarters. I imagine inflation has created tougher comps for this revenue growth source, making it even more impressive. Don’t forget that other revenue sources tend to be much more volatile, making analyzing a trend quite challenging. This volatility is evident in the graph below:

As usual, management shared how Topicus, Lumine, and Altera impacted its organic growth profile. There was not much news on this front for yet another quarter: Topicus is growing the fastest in terms of organic growth, and Lumine the slowest:

Altera, however, continued being a highlight. This is not only important for Constellation due to Altera’s relative size but also because it significantly reduces the bear case that cites that management will not be as good in large acquisitions as it has historically been in smaller ones. During the AGM, management mentioned that IRRs are indeed lower as they go up in the size scale but that the dispersion of returns is also somewhat lower. This means that risk-adjusted returns might be quite appealing in large acquisitions too.

Altera has generated $211 million in Free Cash Flow since being acquired by Constellation. This is pretty impressive considering the company paid an enterprise value of $900 million around a year and a half ago. But these are not the only good news…Constellation has also managed to stabilize Altera’s growth and improve both the margin and cash conversion profiles:

To this, we have to add that organic growth in maintenance and recurring is showing some promise, although it’s still too soon to understand if this trend is permanent.

Looking at expenses

Constellation’s accounting has become less misleading due to the conversion of all the Lumine preferred shares in Q1. The company now shows $0 in the redeemable preferred securities expense, although this will most likely change with the next spinout.

The absence of this expense, together with the following non-operating expense changes, caused net income growth to skyrocket ahead of revenue growth:

Foreign exchange: the company is subject to foreign exchange gains and losses. These are volatile and not an operating line item, so we shouldn’t really take them into account because they should level out long-term.

IRGA membership: this is an expense that comes from the Topicus spinout and is impacted by foreign exchange movements between the euro and the dollar and Topicus’ revenue growth rate

Finance income: I noticed that Constellation seems to have started investing its cash pile, which generated income this quarter, unlike the comparable quarter

All of these were favorable to the company this quarter, and, together with the absence of the expense related to the Lumine spinout, were responsible for the rise in Net income:

It’s not that Constellation suddenly became much more profitable this quarter; it’s just that certain accounting items returned to normal and others favored the company. The redeemable preferred expense is a non-cash expense, so we’ll see later that cash flows have been much more normalized all throughout. Cash flows are the metric that any investor should focus on, more so for Constellation; follow the cash.

There was also some good news in “other, net” which penalized the results. Good news penalizing the results? Yep, this can happen due to contingent consideration. Recall that contingent considerations are payments the company has to make if the investment achieves some pre-determined goals or, in plain English: if the investment is working better than expected. Contingent consideration has been largely responsible for the increase in other, net over the first 3 and 6 months of the year, although I must say that these are not really a significant driver in the grand scheme of things:

The opposite side of the coin (expenses incurred when the investment is not going as expected) is impairments, which have increased quite considerably over the first 6 months. However, as I mentioned some articles ago, we shouldn’t focus too much on the number per se but on its percentage over the total capital deployed. It’s normal to see impairments grow as Constellation deploys more capital, but there’s no denying these are still not worrying, meaning that management tends to be more right than wrong with their investment theses:

Cash flow is the metric to follow, and there’s still some noise

Constellation’s cash flows showed strong growth, but obviously one much more normalized than the accounting numbers. Operating cash flow has grown 33% over the first six months, and Free Cash Flow Available to Shareholders has grown 34%.

Cash flows are seasonal and can be volatile from time to time (especially due to the IRGA liability), so if we focus on the first six months, we can see that the main driver of Free Cash Flow was an improvement in Operating Cash Flow:

A quick look into the company’s operating cash flow shows that the improvement primarily came from improved operational performance. It’s the first time in a while that Constellation’s numbers have been so “clean,” so let’s enjoy it while it lasts!

Acquisitions - Strong quarter again

Constellation continues to do great in terms of capital deployment. The company deployed $624 million into acquisitions during the second quarter (including contingent considerations). Together with the capital deployed in the first quarter, this brings the total capital deployed year-to-date (including contingent considerations) to $912 million, which, together with what the company has already deployed in Q3, brings the year-to-date total to $1.1 billion.

It’s a solid start to the year, but I don’t know if Constellation will manage to beat its record. This is becoming increasingly tough to forecast because large acquisitions are becoming more recurring but are unpredictable.