Bouncing along

Deere’s Q2 2026 Earnings

Last quarter, I ended Deere’s earnings digest with the following:

What this ultimately tells me is that the risk-reward relationship is not as appealing today as it was three months ago (pretty crazy how fast things can change in the stock market). Does this mean that I am going to sell my entire Deere position? Nope, but at the same time I don’t think having Deere with a 7.5% weight (which is an “overweight” position judging by how my portfolio is distributed) makes sense with this risk reward. For this reason, I have sold some of my Deere stake today and will redeploy the proceeds over time to other things that I believe offer a better risk reward.

Now, I could perfectly be wrong and Deere might continue compounding from here at rates that I can’t even fathom right now. This said, most of the times when I have not trimmed unappealing risk-rewards, I ended up regretting it. I wouldn’t probably cut Deere were it not for the fact that there are other very appealing risk-rewards across the portfolio. Can the stock continue going higher? Of course, Deere today has one of the best things one can have in the market: momentum.

The shares were doing great back then thanks to the expectation of an imminent inflection point and momentum, but the reality was that the business was not yet inflecting materially (the market tends to anticipate inflections). I partially sold my stake at $647, but the shares are trading today around 20% lower, which begs the question: is Deere a good opportunity again?

The goal of this article is to (a) provide an overview of Deere’s most recent earnings, and (b) update the valuation exercise to understand whether Deere is again an attractive opportunity. Recall that you can read my Deere in-depth report for free here and access more than 8 updates here.

Without further ado, let’s get on with it.

Deere’s Q2 earnings

I would characterize Deere’s most recent earnings as “uneventful” despite the market’s reaction (the shares dropped around 5-6% following the release).

Q1 earnings (the prior earnings) were stronger than expected and management voiced their optimism around 2026 being the bottom of the large ag cycle in North America, but Q2 earnings were weaker and came with a more cautious management team. This probably made investors worry about a potential deterioration of the industry, which presented itself in large ag.

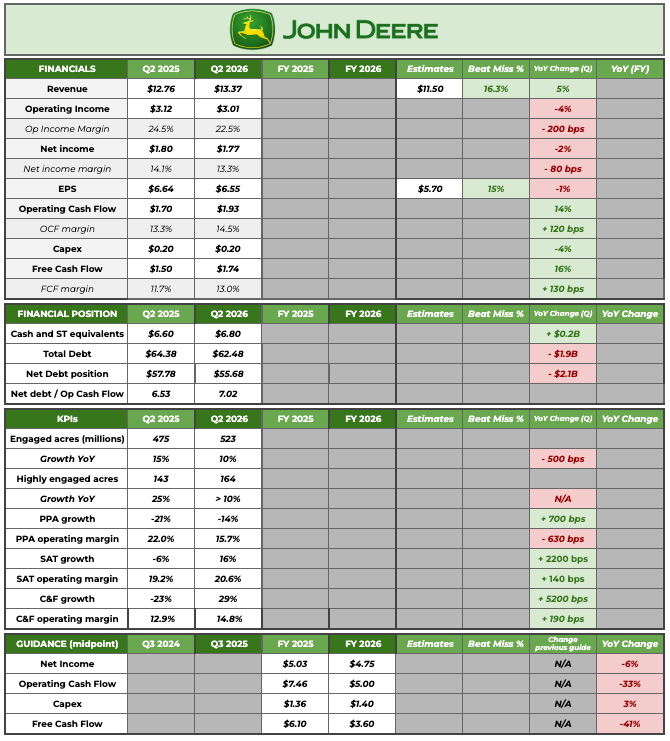

Before going into more detail, here’s Deere’s summary table:

Deere reported its third consecutive quarter of top line growth despite large agriculture still humming along the bottom of the cycle. The reason is diversification: Small Ag & Turf and (especially) construction are doing pretty well. Management believes that the three segments are currently in very different stages of the cycle with two of these still being below mid-cycle (PPA and SAT):

While Large Ag is operating below trough levels, Small AG & Turf is progressing toward mid-cycle, and Construction and Forestry is slightly above mid-cycle.

Deere definitely needs large ag to recover, but there were also several good news on the Large Ag front. Despite an expected significant deterioration in the ag industry due to the conflict in Iran, Deere maintained its expectations for large ag in North America, raised those of APAC, but significantly lowered those of Brazil. Let’s try to unpack this a little bit.

The conflict in Iran has created a surge in fertilizer prices, which has a more significant and immediate impact on Brazilian farmers. The main reason is that there are more harvest seasons in Brazil and therefore farmers are more exposed to fertilizer spot prices.

The situation in Iran is affecting Brazilian growers at a particularly sensitive point in their production cycle as they prepare to plant a new crop in the September timeframe. While farmers in other parts of the world have largely locked in inputs for this growing season, Brazilians have more exposure to current spot prices.

Higher fertilizer prices are bad for the industry, but might even be a net positive over the medium/long term for Deere. When fertilizer prices go up, crop yields go down because farmers use less fertilizer but plant the same acres. This eventually makes crop prices rise (somewhat protecting farmer profitability). Over the long term, I believe it also makes farmers more open about adopting technology because certain Deere products offer significant savings in inputs.

Despite the relative weakness in large ag, I believe there were two highlights:

Deere did not change the full year guide despite the conflict in Iran, which I’d say not many people expected. I’ll discuss later why this might have been the case

Despite doing worse than expected and being below trough-cycle levels, equipment operating margins in large ag remain above double digits (including in Brazil)

So yes, not the best environment for large ag, but still a pretty profitable business for Deere. There is also good news in terms of the potential recovery. First, management alluded to new biofuel regulation potentially becoming a significant tailwind for corn demand:

The house recently passed year-round E15, which we view as a positive step forward. Today, roughly one-third of US corn production goes to ethanol, and broader E15 adoption could, over time, meaningfully expand corn demand as blending infrastructure comes into place.

This should give you some context on what this means:

Historically, standard U.S. gasoline is E10 (10% ethanol, 90% gasoline). E15 increases the ethanol blend to 15%. However, under a literal reading of the 1990 Clean Air Act, E15 has been banned in roughly half the country during the summer driving season (June 1 to September 15) due to archaic regulations surrounding fuel volatility and summer smog. To keep E15 flowing in recent summers, the EPA has had to issue emergency, temporary waivers. The bill passed by the House aims to permanently remove the summertime restriction nationwide, giving fuel retailers the legal certainty they need to invest in E15 pumps without fearing a sudden summer shutdown.

This seems more like a longer term demand driver, but management also believes there is significant replacement demand coming sooner:

We’re a couple of years into the downturn. We’ve seen less replacement. We’re seeing age of fleets continue to grow. As we track this in North America, we’re at very elevated levels for high horsepower tractors. Very elevated levels in terms of fleet age for combines as well.

Higher demand should result in higher volumes, which together with tariff costs unwinding should bring considerable operating leverage (already apparent in non-PPA segments), but then we also have to add higher tech penetration (which evidently brings higher margins). There were several interesting tidbits on this front:

Engaged acres increased 10% YoY

Highly engaged acres increase by more than 10% YoY

Monthly active digital users are close to 440,000

Precision essentials renewal rates for 1 year customers is 70%, for second year customers is over 90%. This means that those who find value stick with it

Now, all of the above allowed Deere (despite PPA not doing great) to maintain the full year guide but I’d argue there was some sort of implicit lowering of the guide. The reason is that Deere recovered around $300 million from the IEEPA tariffs (like Keysight), which means that the actual net tariff impact this year is closer to $900 million than $1.2 billion. With the guide unchanged this means that it’s implicitly $300 million lower, that management is being considerably more conservative (we’ll only know in hindsight), or that the impact of the Iran conflict was softened by the tariff tailwind. Now, I would say this is not a bad outcome considering that large ag (Deere’s most important segment) is expected to remain in a downcycle through FY 2026.

So, what will we get in (potentially) the last year of the downcycle? Management argued that they expect H2 revenue to be slightly ahead of H1 revenue. H1 revenue was around $22.98 billion (+8% YoY), so let’s assume that H2 revenue comes in at $23.5 billion. This implies a 3.6% revenue decrease in H2, or a 2% growth rate in FY 2026. Not great, but not bad either considering it should be the trough year (we’ll see). At $5 billion in net income, that would result in an 11% net income margin, which is pretty acceptable considering tariffs and the stage of the large ag cycle.

Let’s take a look at the valuation.