Best Anchor Stocks 2023 Annual Recap

Brief market commentary, overview of the portfolio, performance, lessons learned...

The premium subscription gives you access to all the content in Best Anchor Stocks, which includes…

All the deep dives

Recurring articles

Access to my real-time portfolio and transactions

Occasional webinars on various topics

A community of like-minded investors

A subscription the Premium + also gets you a quarterly Q&A with me to discuss anything you’d like.

If you want to know the type of content I share at Best Anchor Stocks you can read the Deere deep dive I uploaded a few weeks ago for free…

…or you can also read any of the other many free articles I have shared, just like this one!

You can also read the testimonials that existing subscribers have left. If you are a passionate and curious investor wanting to learn about high-quality companies, don’t hesitate to join Best Anchor Stocks!

Hi reader and welcome back to the Best Anchor Stocks blog,

It’s been around two years since Best Anchor Stocks was launched, and I thought it would be a good idea to write an article reflecting on these years, and obviously in 2023 more specifically (that’s why it’s called the “annual recap,” after all). Some of you might know that I left my full-time job in consulting to run Best Anchor Stocks, and I must say that it was a great decision despite it feeling quite risky at the beginning. I now work in my passion and have greatly accelerated my learning curve (something that I will talk about later on).

This recap will discuss the following topics:

The market in 2023

An overview of the portfolio

Performance

What I have learned this year

One thing I will do differently in 2024

I hope you enjoy this article as much as I enjoyed writing it. Without further ado, let’s get on with it.

The market in 2023

I won’t overextend myself in this section because there’s no need to. Most long-time subscribers or people who have been following me for a while know that I don’t care too much about the market/macro in any particular year. This said, let me share some brief thoughts.

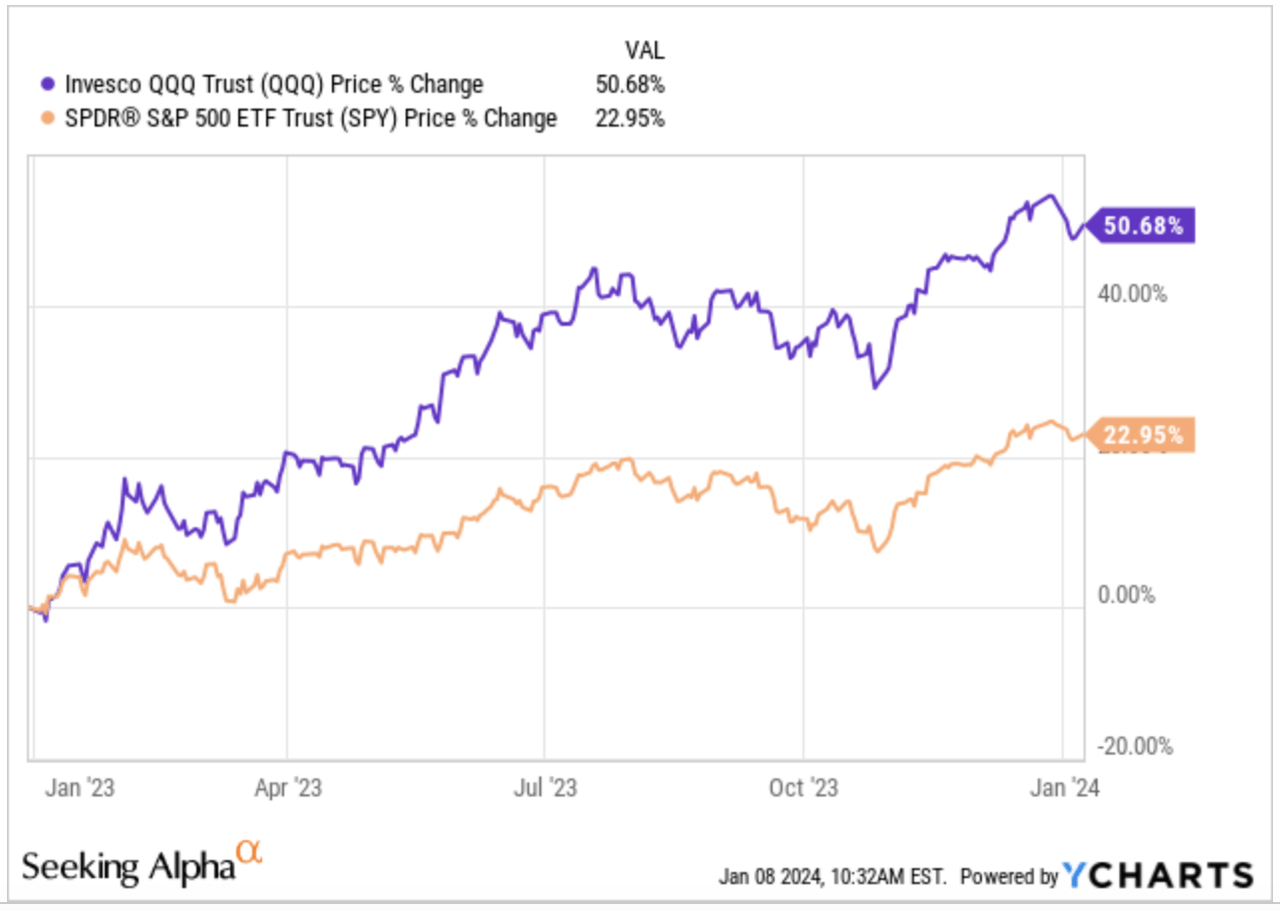

In my opinion, the main takeaway in 2023 was that we can’t forecast macro and, thus, should not waste time doing so. Every economic variable seemed to be a headwind coming into the year: indices were significantly off ATH, interest rates were rising, inflation was running hot, geopolitical conflicts…but despite all of these, the indices were able to post an outstanding performance:

Of course, you’ll now see many people claiming that they saw this coming and that it was evident, but that’s an easy claim to make in hindsight. The reality is that recency bias reigned in December 2022, but those people exposed to this bias have been proven very wrong this year.

Forecasting macro is futile because thousands of variables come into play in the economy, more so if one considers that we now live under one global economy. The thing is that forecasting macro is just the first step a market timer must get right. If and only if a market timer gets the macro right, they will also need to get the market’s perception right to make money; oh! And also get the timing right. It's not an easy task by any means. I always found it interesting how market timers tell fundamental analysts that forecasting fundamentals many years out is impossible (granted, it’s tough) but that forecasting macro next year can be done. Worth noting that two of the institutions that can exert significant influence over the economy (Central Banks and Governments) have no clue what will happen next year. This pretty much tells you how complex economic forecasting is.

Needless to say, knowing that one can’t forecast macro does not mean that one should ignore macro or that macro doesn’t matter. Evidently, the economic landscape where companies operate matters for their results. A good approach (or at least my preferred approach) to avoid worrying too much about macro is building a portfolio of companies that enjoy secular tailwinds and are well protected if a recession comes (easier said than done, of course). I think most of the companies in my portfolio comply with this characteristic, so I am not really worried about a potential downturn. I’d go as far as to say that a recession could benefit these companies because they face weaker competitors.

All in all, it was a year marked by inflation and macro, although it did not go the way many people thought it would. Macro forecasters 0 - 1 Macro agnostics. I don’t think I need to say what team I belong to.

I have recommended this book several times throughout the year to my subscribers:

It might not appear helpful from the point of view of a long-term investor, but I think it’s excellent to understand what moves prices over the short term. I don’t want to spoil anything, but I can tell you it’s not fundamentals. Always worth keeping this in mind before rushing to conclusions following a price drop.

An overview of the portfolio

I made 4 additions to my portfolio this year to end up with 14 companies. The companies I incorporated belong to the following industries: healthcare, entertainment, spirits, and luxury (this is true luxury I must say).

I receive the following question on many occasions:

How many stocks are you willing to hold in your portfolio?

I have always thought that a number between 15 and 20 made sense for me. I believe this would give be enough diversification while at the same time being manageable to follow closely. I don’t think the number per se is as important as the quality of the companies included in it and how unrelated (or related) they are between themselves. I mean an investor is much more diversified owning Constellation Software (which caters to hundreds of industries) than owning 10 financial companies.

It was obviously much more challenging to find ‘deals’ this year (especially in the second half) than in 2022, when everything was out of favor, but I think these were great additions. Some of these companies have also been out of favor in 2023. Investors are not too fond of the healthcare and spirits industries, but I believe they are excellent businesses to hold long-term, and it’s just a matter of time before market perception changes.

These were new additions to the portfolio, but I also kept adding to many of my positions throughout the year. I added to 9 out of the remaining 10 positions. The only exception was Constellation Software, and that was for two reasons:

As I discussed with subscribers when I included Constellation in my portfolio, my inability to purchase fractional shares made me build a significant position from the get-go.

Constellation currently makes up 17% of my portfolio. I don’t want to be too overweight in any particular company (as I could always be wrong with an investment thesis). Still, I believe Constellation will remain the number 1 position in my portfolio for a long time.

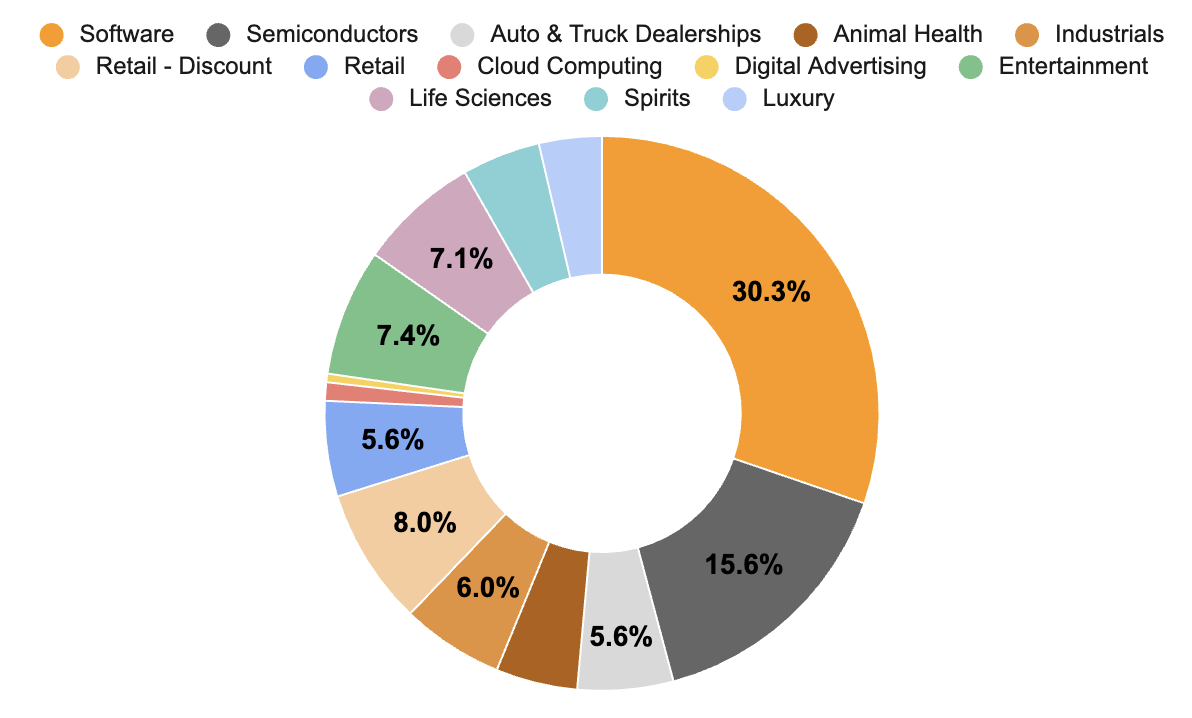

The portfolio ended the year distributed as follows across industries:

Just looking at this chart, one might think that I am too concentrated on software, but there’s a caveat: Constellation software makes up more than half of the software's weight. I don’t have anything against software, but I think the disruption risk is much more significant there than in other industries. As most of you know, I care a fair bit about durability, especially when paying up for businesses.

I believe all the industries I have exposure to are secular growers. One of the lessons that I learned this year is to remain open-minded when it comes to industries. I tend to focus quite a bit on the economics of any given industry because I believe it will be a significant determinant of future returns. This chart by Mauboussin exemplifies why. In short, it’s easier to make money in industries with favorable characteristics for value creation:

There’s a very recent example of this open-mindedness in a recent article I published for subscribers, where I discuss two industries I thought I would never like. I considered these industries commodities, but a further look changed my mind. As François Rochon said in my interview with him this year (this interview was another annual highlight, by the way):

It's really case by case, again. We don't really focus on industries. We focus on companies and trying to find companies that we believe have something special.

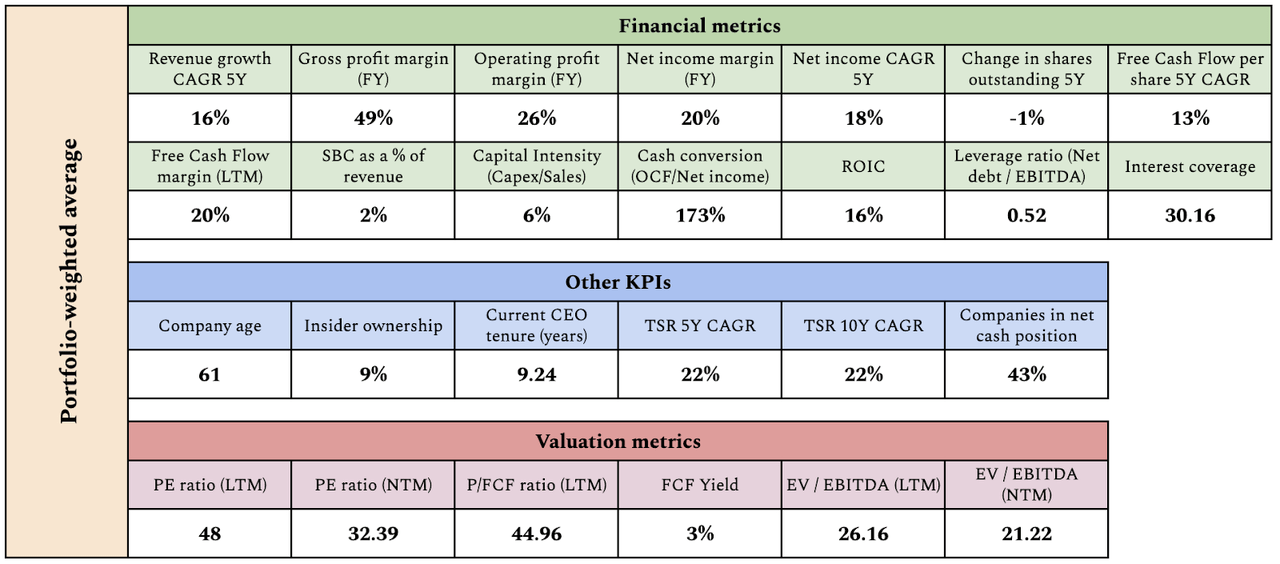

I recently built a quality table for my portfolio (idea is from Terry Smith), from which we can get several interesting insights:

First, I think it’s pretty clear that my portfolio is made up of high-quality companies (great growth, margins, returns, and low leverage). Of course, these numbers are based on the past, but that’s simply a consequence of our inability to calculate them looking forward. That’s where the qualitative work should come in: to ensure that the numbers continue to look similar or even better in the future.

The KPIs also have some interesting insights. The portfolio is made up of relatively old and established businesses whose stock has enjoyed great performance in the past. Past performance is never a perfect proxy for future returns, but if an apparently great company has not done well in the past, this might be because:

The company is not as high quality as one would think

Management does not know how to translate that quality into shareholder returns

None of those are great signs, although we can encounter some cases where the future might look strikingly different than the past. We should be aware, though, that these cases tend to be the exception rather than the rule. As Warren Buffett brilliantly said:

Turnarounds seldom turn.

Then, if we look at the valuation metrics we can see that my portfolio is more expensive than the market as a whole. Terry Smith shared in his recent annual letter that the media FCF yield for the S&P 500 is 3.7%. This metric lies at 3% for my portfolio so it’s obviously more expensive than the median company in the index.

My portfolio definitely trades at a premium, but I did not expect different when going for companies that are significantly higher quality than the market and that are (in my opinion) very durable (durability is crucial, and I’ll talk more about it later on). There’s a drawback, though: quantifying the difference in quality is almost impossible so on a quality-valuation basis it’s tough to gauge if the portfolio is cheaper or more expensive than the index.

Performance

Before talking about annual performance, I want to clarify that the only performance that really matters is Inception To Date and the CAGR one has generated since that moment. Many investors focus on YTD (Year To Date), QTD (Quarter To Date), or various time frames, but I don’t think those matter much because they will always be cherry-picked.

This said, I also believe that we need a sufficiently large period to judge performance. As I see it, this period is at least 5 years or an entire economic cycle. Only after such a period will one be able to distinguish luck from skill, and maybe not even then.

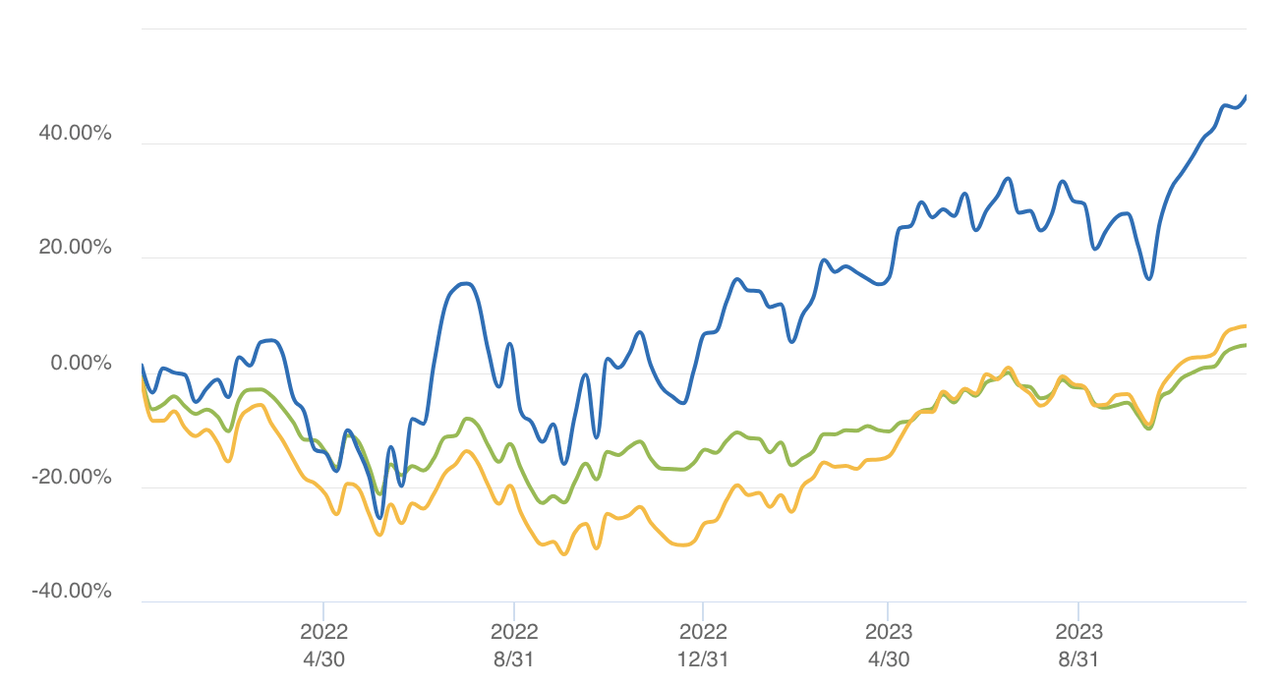

My portfolio (blue) performed well in 2023, outperforming the S&P500 (green) by a good margin but significantly underperforming the Nasdaq (yellow). It returned 37% in 2023, which is (or at least I consider) excellent:

One of the reasons why showing year-to-date returns is a bit misleading is that it misses where we come from. 2023 was a great year for almost everyone (it was relatively easy to make money this year), but 2022 was a different story. My portfolio has done well since inception (14th of January 2022), significantly outpacing both indices:

The portfolio has produced a Money Weighted Return (‘MWR’) since inception of 48.3%, or what’s the same, a 21.7% MWR 2-year CAGR. Of course, this looks great and I am very happy with the performance, but as I said earlier, I think we must judge this performance when we have at least 5 years of track record, not less. The stock market can be one of the most dangerous places on earth to lie to ourselves.

Another thing worth noting is that the portfolio’s benchmark might need some tweaking. I am currently benchmarking my portfolio against the US indices, but I might need to change that for the MSCI world because my portfolio is comprised of companies from all over the world. I currently own companies from the US, UK, France, Netherlands, Japan and Canada. Anyways, I don’t think I’ll get too obsessed with the benchmark.

I have also talked about the concept of risk-adjusted return this year. Returns are somewhat straightforward to calculate. They are quantifiable. Risk, on the other hand, is not. This brings a problem because the metric that every investor should optimize for is risk-adjusted returns, but we can only calculate one of the sides of the coin. Of course, I am not going to bring a way here to calculate risk (volatility is not the way, FYI), but I will tell you that I do believe my portfolio has somewhat low risk if we take the probability of a permanent loss of capital as a proxy to risk. I am confident that my success as an investor will come more from minimizing my permanent capital losses than from outperforming the benchmarks in a year when everyone has made money!

What have I learned this year?

This has been yet another full year in which I have been able to “work” full-time in my passion. That has, of course, greatly accelerated my learning curve. I have learned a lot of things this year, but I would like to talk about two briefly.

The first one is the importance of durability. When investing in high-quality companies that typically trade at apparently rich multiples, one must focus all of their efforts on how durable those cash flows will be. Forecasting the future precisely 10 years out is almost impossible, but we can focus on analyzing the characteristics that make a company and its competitive advantages durable. I have recently written an article on this topic, which I am increasingly focusing on.

The second lesson learned is also related to durability: focus on supply. Many investors tend to focus on demand because it feels natural, right? If I want to understand how a company will grow, I must focus on the demand for its products/services. This obviously makes sense, and focusing on supply does not mean disregarding demand, but supply has become increasingly important in my investment process. The reason is two-fold:

Supply is what makes a market attractive: if there’s excess supply, then the suppliers will not enjoy great economics.

A controlled/capped supply is what makes a company durable: it’s much easier to forecast the future of a company that operates in a supply-constrained market than it is to do so for a company where the supply landscape is uncertain.

This week I read the shareholder letter (one of the best I have read) of a company I am currently analyzing where the management team said the following:

The competitive dynamics of scarcity can be very powerful.

I completely agree with that quote and I think it’s something that should be in every investor’s mind.

These are only two of the many lessons I have learned this year. We should never forget that we live in a constant learning process as investors.

One thing I will be doing differently in 2024

One thing I will be doing differently in 2024 is not limiting what market caps I am looking at. When Kris and I launched Best Anchor Stocks two years ago, we decided to focus on high-quality and stable businesses to help reduce the volatility in one’s portfolio. The rationale behind this is that, despite volatility not being a risk, it does expose investors to one of the most significant risks of all: heightened activity. These established businesses tend to have larger market caps, but instead of this being a consequence of the companies I look for, I think I made it a requirement.

I don’t think high quality is a characteristic inherent to any market cap level, so this year, I will also be looking into high-quality, smaller-cap companies. There are plenty of them, and the good news is that they tend to be out of the spotlight and out of reach for many funds, and thus, they tend to be cheaper than they should (not always, of course). Companies can have small market caps for a lot of reasons, but a small market cap in itself says nothing about a company’s quality.

All this said I don’t believe that market inefficiencies only belong in the small/mid cap space. If 2023 has proven something besides the futility of macro predictions it’s that there can be market inefficiencies even in the largest companies in the world. The key (in my opinion) lies in the compensation structure of the industry which forces many institutional investors to focus on the short term. I know many people will not agree with this take, but there are many large businesses that have been greatly misunderstood by the market at times.

Conclusion

All in all, I hope you enjoyed this article as a 2023 recap. I believe 2024 will be a great year (optimism always reins in me). I am getting married this year, I am very grateful to work in what I love, and I am also grateful for the great community we have built at Best Anchor Stocks. Thank you for your continued support!

In the meantime, keep growing!

Really enjoyed reading your letter Leandro and congrats on a great performance. Best wishes for 2024.

Great read Leandro and congrats on the returns.