Adobe’s Identity Crisis: Growth Stock or Falling Knife?

The $6.4 billion quarter nobody trusted

If you’ve been following Best Anchor Stocks for a while, you’ll know that I have held Adobe for some time (with only the sizing of the position changing all throughout). A couple of weeks ago, I shared my decision to sell the position with subscribers. The reasons behind this decision could be summarized in the following:

AI capabilities have advanced quicker than I previously envisioned and it will take some time for Adobe to disprove the narrative (I was wrong here)

With many opportunities across the portfolio, I felt there were better places to put my money in (this is a result of the current market context more than anything specific to Adobe)

The above doesn’t mean I have stopped following Adobe or that I have completely discarded owning it ever again, as I am well aware that I could’ve made yet another mistake selling my shares (wouldn’t be the first time!). I’ve sold 5 shares before selling Adobe, 4 went on to languish, whereas one more than doubled from my selling point. What’s difficult about this game is that I don’t know where Adobe will fall and I’ll only know with the benefit of hindsight.

Last quarter, the company reported Q1 2026 earnings and announced that Shantanu Narayen (18 years at the helm) would be transitioning from the CEO position. My goal with this article is threefold: go over the earnings highlights, share some thoughts about the CEO transition, and explain what I believe are the main components of the bull and bear cases. Regardless of whether you are an Adobe bull or bear, my hope is that this article helps fill your blind spots.

Without further ado, let’s get on with it.

Adobe’s excellent (?) earnings (and what the market is worried about)

If there’s one thing that has remained a recurring overhang for Adobe’s stock (and the stocks of software companies in general), that’s the AI risk (hopefully not discovering anything new here). Even though Adobe was not capable of completely eliminating this overhang last week, I do think it was suffered in a different “environment,” one in which most of Adobe’s KPIs accelerated (just not the one that the market seems to be fixated on).

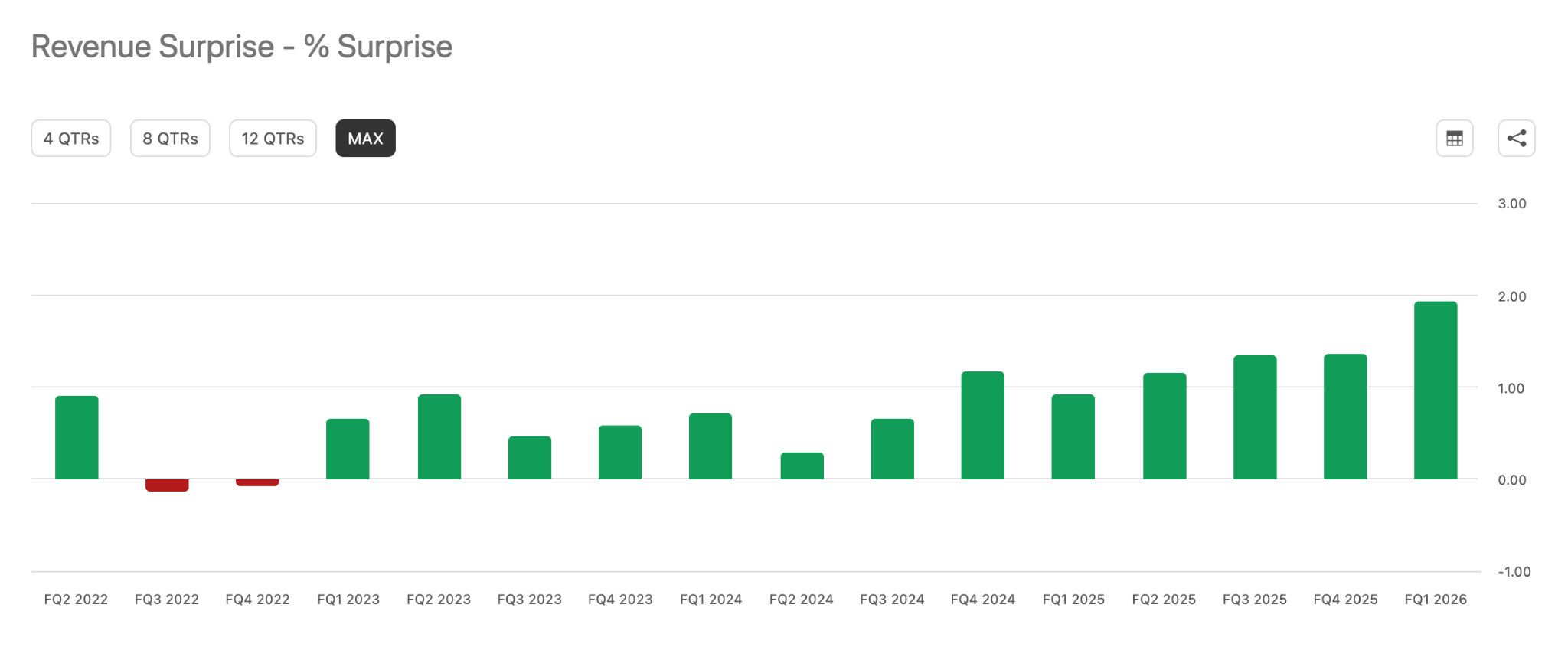

Adobe reported (for the first time in a while) an apparently flawless quarter, significantly beating analyst estimates and providing little firepower for algos to demolish the shares. Let’s take a look at the top line, which seems to be the only thing that the market cares about (and maybe rightly so).

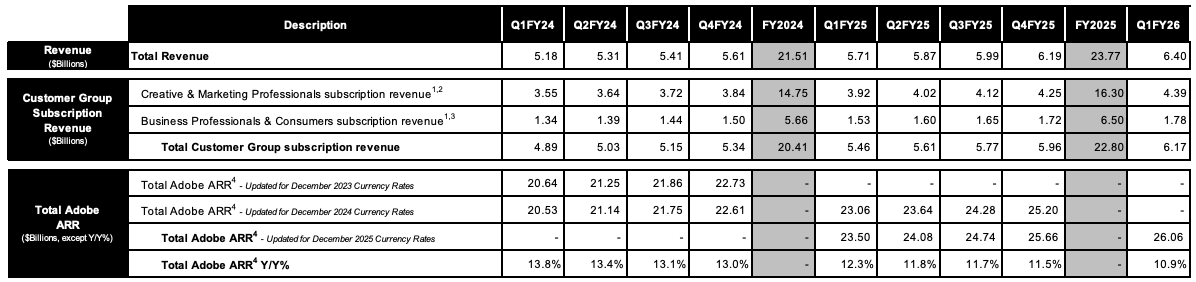

Adobe reported Q1 FY 2026 revenue of $6.40 billion (+12% YoY), significantly beating consensus estimates of $6.28 billion. It’s kind of interesting that Adobe’s most significant beat over the last 4 years has taken place during the AI era (narrative violation? Or maybe a mix shift?):

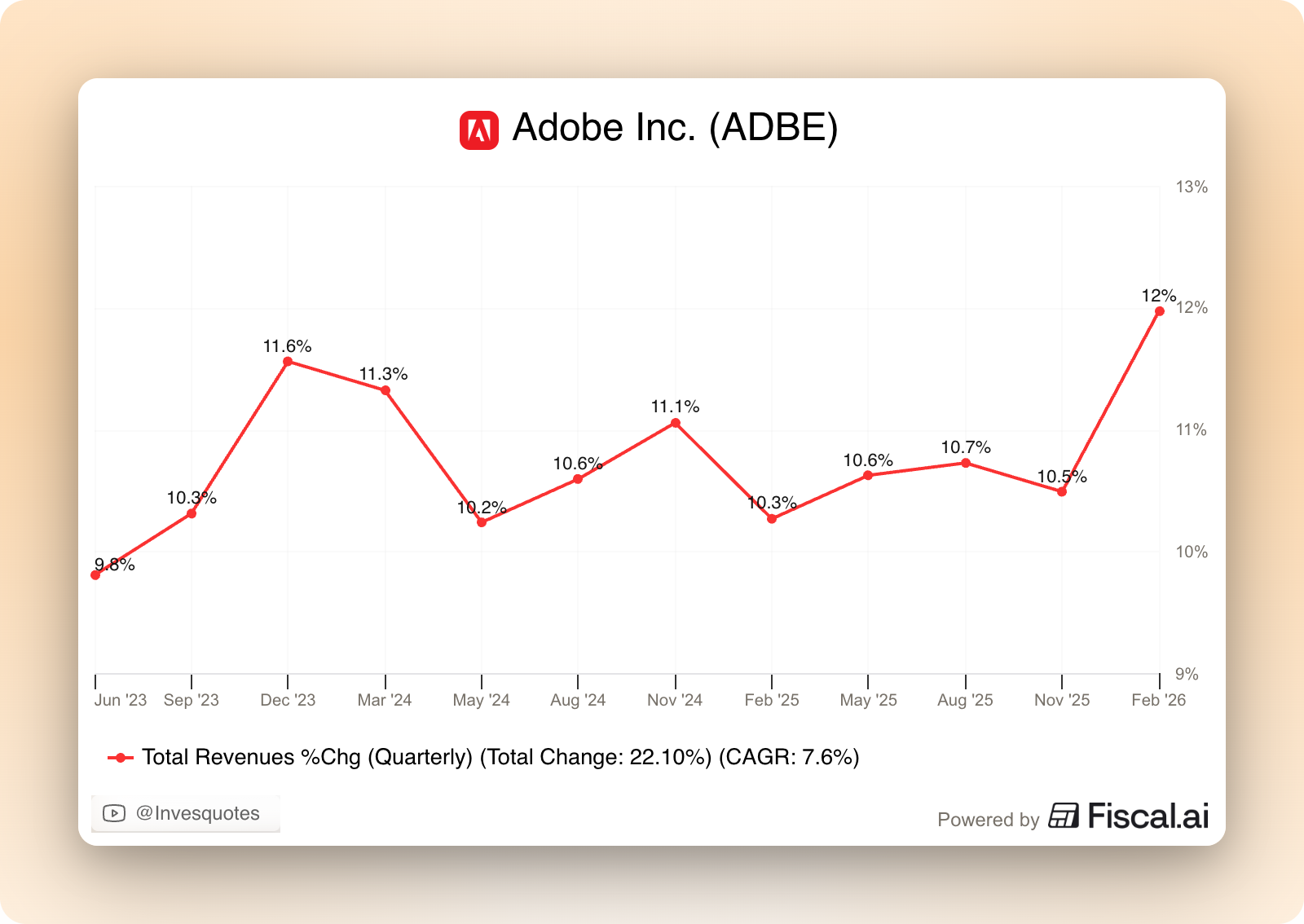

Adobe not only beat estimates significantly but also showed for the first time in a while a clear acceleration in its top line:

Just so you can gauge how investor sentiment has shifted for Adobe, consider that December 2023 was the last time Adobe was growing at a similar pace, with the non-minor difference that the stock was trading at an EV/EBIT of 43x, compared to today’s EV/EBIT of 11x. One could argue that low double digit growth did not deserve a 43x EBIT multiple, but what’s undeniable is that (absent a significant difference in growth) Adobe has gone from loved to hated.

Now, the company’s growth needs some context. For starters, a greater portion of the company’s revenue is becoming consumption/usage-based rather than pure recurring revenue. Even though I don’t think this is necessarily bad, it undoubtedly makes revenue growth more volatile and likely makes it tougher to identify a trend from just one quarter.

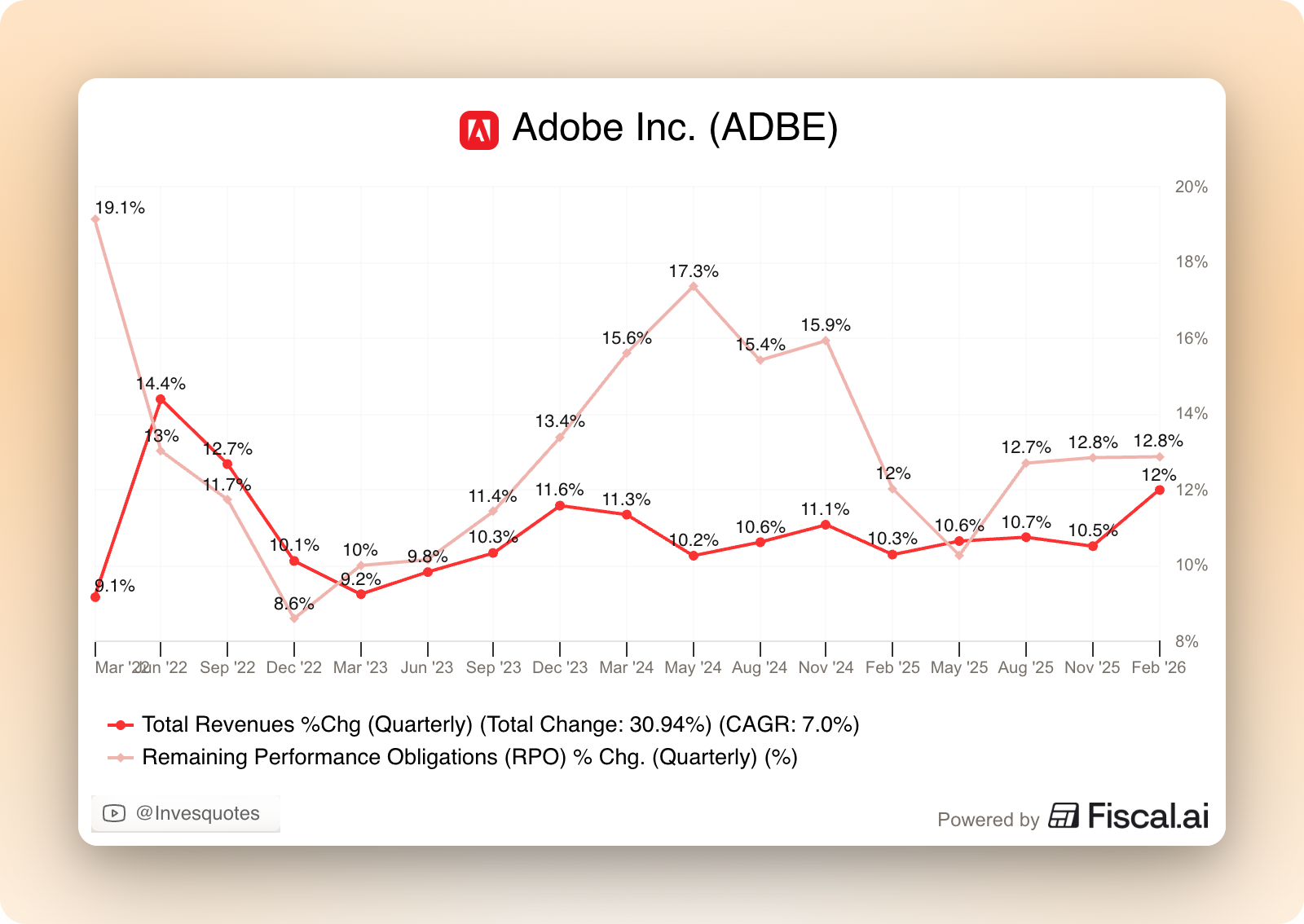

The “good” news is that Adobe has several leading indicators an investor can look at to understand how healthy the business is barring consumption trends. Two metrics are worth highlighting here: RPO and ending ARR. RPO (Remaining Performance Obligations) continued to grow at a good pace. Despite having decelerated from peak levels, RPO has proven resilient and continues to grow ahead of revenue:

Adobe’s core business is pretty resilient, so there’s an argument to be made that any kind of AI disruption thesis would most likely present itself to a greater extent in this metric before showing up in revenue.

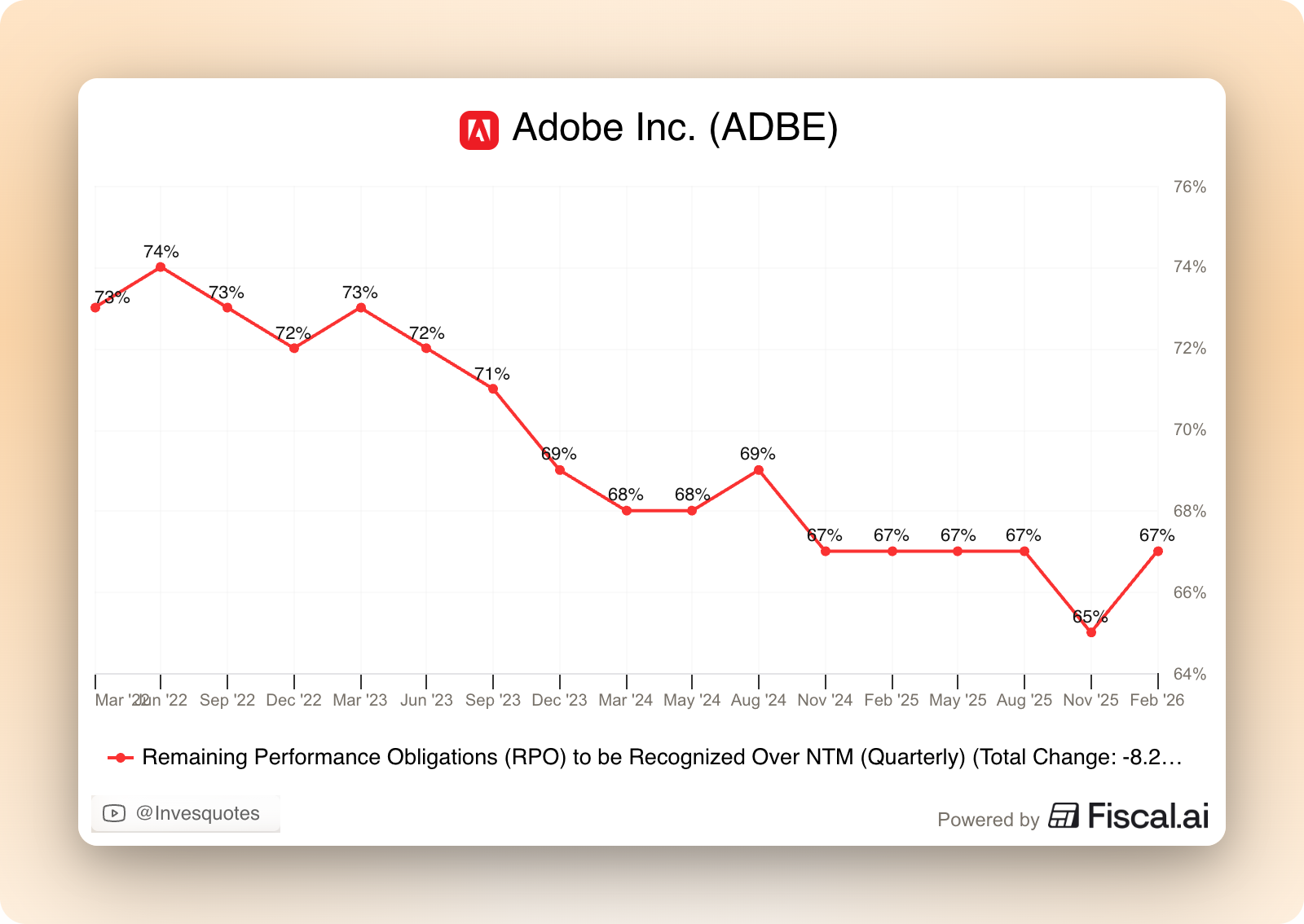

The interplay between Current RPO and total RPO is also interesting and portrays how Adobe’s business has shifted over time. Remaining performance obligations to be recognized over the next twelve months (i.e., Current RPO as a percentage of total RPO) has ticked down relatively fast:

This should not surprise anyone. Management has been pretty vocal about its One Cloud strategy and how it’s a tool to become the strategic partner of enterprises. This enterprise focus has made enterprises become a more significant portion of the business over time and one could argue that this is part of the bull case (I’ll share some thoughts on this topic later on) because it lengthens Adobe’s runway. I would say, though, that Adobe’s RPO number doesn’t even make up one year of revenue.

Now, I believe it has become obvious that what the market is worried about is not RPO, but ending ARR growth. Ending ARR growth has decelerated through 9 consecutive quarters:

Source: Adobe Investor Data Sheet

There’s no immediate trend reversion expected either considering that management maintained the ARR growth guide for the full year at 10.2%, 70 bps below the first quarter’s result. The first thing that should come to mind here is the following, which is also a great segue into understanding how Adobe’s business has shifted/adapted over time:

Why is RPO proving resilient while ARR is decelerating?

The answer to this question is relatively straightforward: these metrics measure different things across different time horizons. RPO includes multi-year commitments whereas ARR only takes into account the next twelve months. This makes ARR a much “better” leading indicator of next year’s revenue (although Adobe claimed that RPO conversion to revenue should not differ materially from what it has been in the past) and therefore it has become what Wall Street is focused on.

It’s worth noting that consumption-based revenue bypasses the ARR figure entirely (as it’s a usage-based metric). This means that revenue growth can temporarily detach from ARR growth, something that may become the norm in the future as AI-usage ramps across Adobe’s tools.

Wall Street has two options in this new “AI era:”

Acknowledge that ARR is less useful as a leading indicator as usage-based revenue streams ramp up

Believe that ARR growth will tick up as management monetizes new users (i.e., management’s explanation)

Management shared two explanations for the slowing ARR growth, one of which I believe makes sense and one of which I believe should be taken with a grain of salt. The one which makes sense is the freemium model, although it did not precisely calm investor fears. Management argues that, as Adobe rolls out AI features and goes downmarket, the sales process becomes longer as it involves making customers use the tools extensively and then paywalling features down the line. This means that ARR growth might potentially slow down despite usage indicators being at ATHs (all time highs):

We saw tremendous MAU growth in our new initiatives that dampens ARR in the short term but sets us up to deliver in the quarters ahead.

How we route that traffic to freemium offers is going to be really the evolution that Shantanu is talking about in terms of the change that we should expect to see. As that traffic goes to these new offers, it’s just going to take a little time for them to use the product, to hit the paywalls and then translate out. Again, as we’ve said on the prepared remarks, this is really a strategy to drive MAU, drive credit consumption, drive enterprise usage, and we should expect to see that start to accelerate in the back half.

One could definitely give management the benefit of the doubt here, but with the market being in “shoot-first-ask-questions-later” mood this does little to tame the monetization fears. Ultimately, the market believes that AI will translate into higher usage of Adobe’s tools, but that conversion may somewhat languish due to increased competition/alternatives (in the non-professional side at least).

The second reason management shared to explain the decelerating ARR growth was the declining Adobe Stock business:

While Q1 had many highlights, our traditional stock business saw a steeper decline than we expected. This shift is playing out more quickly than we had planned for, and our focus remains on giving customers meaningful choice between stock and generative AI as they build their creative and marketing workflows.

Ending ARR would’ve grown 11.2% ignoring this segment, 30 bps above the reported 10.9%. This would’ve still been a deceleration, but not to the same extent. I don’t really “buy” this explanation because I do believe that the Stock business is most likely a terminal 0 in a world of generative AI. Now, this doesn’t mean that the underlying shift from Stock to Gen AI subtracts from Adobe’s total opportunity. Adobe should theoretically be compensated through higher consumption-based business and better retention as AI tools are rolled out across its apps.

The bottom line is that, in this new generative-AI era, ARR might just be a less appropriate indicator of Adobe’s health, although one Wall Street is likely to continue focusing on. So, yes, the decelerating ARR growth can potentially be “worrying” and is likely what the market is focused on, but we must understand that businesses shift and adapt and Adobe is no different.

There were also several positive and more qualitative indicators that portrayed that the business is doing very well in terms of top of the funnel. Let me share a couple of these…

AI-first offerings ending ARR tripled year over year. While this looks good, we should not forget that AI-first ARR is still a very small portion of total ending ARR (around $250 million on a $26 billion total ARR base)

The top of the funnel continued growing at a good pace with 850 million MAUs growing 17% year over year and with Creative Freemium MAU crossing 80 million and growing 50% year over year. Note that the market’s concern is likely not how many MAUs AI can bring into Adobe’s franchise but more so how monetizable these are in an AI-first creative industry. The fact that ARR growth is decelerating as MAU ramps up only serves to confirm the market’s POV (until proven otherwise)

Enterprise contracts also grew at a good pace

I believe that these qualitative indicators don’t do much in terms of disproving the bear case. Yes, AI is driving usage across Adobe’s tools and, but this doesn’t mean that it will be a profitable endeavour for Adobe over the long term. As an Adobe bull/bear, one has to try to understand not only whether Adobe’s top of the funnel is getting larger (it is) but whether conversion will remain at the high level it has been in the past (this is still not as clear and the ARR growth slowdown does not tame fears).

A poorly communicated transition

Besides slowing ARR growth, something that probably spooked the market was the announcement of Shantanu Narayen’s departure. I don’t think it was THE FACT per se that spooked the market, but rather the HOW: Adobe doesn’t have, at this time, a successor for Shantanu and has opened up the search to external candidates. This seems like a very strange thing to do for several reasons. First, many (myself included) thought that David Wadhwani (Head of Digital Media) was the obvious and natural replacement. He has been driving the AI strategy in Digital Media so it’s honestly strange to not see him as a candidate (maybe he is, who knows). Secondly, it leaves the impression (doesn’t necessarily mean this is the case) that Shantanu decided to jump ship during this “disruptive” period for Adobe. This should somewhat add to the fears that not many insiders have been buying shares in the open market despite spending billions of shareholder money in repurchasing shares (which I am not saying is wrong).

I only have two explanations for this. First and probably more plausible (Occam’s Razor): Adobe simply made a communication misstep. Second and maybe less probable: the Board believes that David missed the AI-pivot and therefore they don’t think he is the right fit. Either way, it leaves Adobe in a tough spot. Investors might now believe that there’s nobody at the helm in precisely the period where Adobe needs someone at the helm. If the board ends up choosing David, it leaves the impression that they went out to look for something better but could not find it. I don’t think that this episode will matter LT so long as the new CEO is the right fit, but when the stock is trading where it is, it’s something that Adobe can’t afford. Another potential explanation is that Adobe might have wanted to get this over with after reporting a pretty good quarter.

We’ll only find out in hindsight.

Adobe’s bull and bear cases (food for thought)

Like for any other company, there’s a bull and a bear case for Adobe. Judging by the stock’s performance and sentiment surrounding the name, I do believe that the bear case is much louder today than the bull case, which doesn’t mean there’s not a bull case. In this section I’ll go over what I consider to be the bull and bear cases. Let’s start with the good news for Adobe shareholders.

The bull case

Even though many Adobe shareholders use the past to portray the bull case (since 2016 FCF per share has CAGRd at a 22% clip whereas the stock has only CAGRd at an 11% clip), I believe the argument misses the point. While it’s sometimes THAT easy, one can’t deny that Adobe faces a terminal value risk that the numbers have not yet been able to disprove entirely (see my commentary on ARR growth above). Now, this doesn’t mean that it can’t be a good investment opportunity today. For one, Adobe is trading very cheaply if one believes that AI doesn’t permanently impair the business, and there are reasons to be positive going forward. My bull case rests on the following four pillars…