Acceleration inbound and optionality abound

Amazon’s Q1 2026

Last quarter, I concluded my Amazon Q4 update (where I also made the case for Big Tech) with the following:

I am considering increasing my exposure to Big Tech, and I’ll keep you posted.

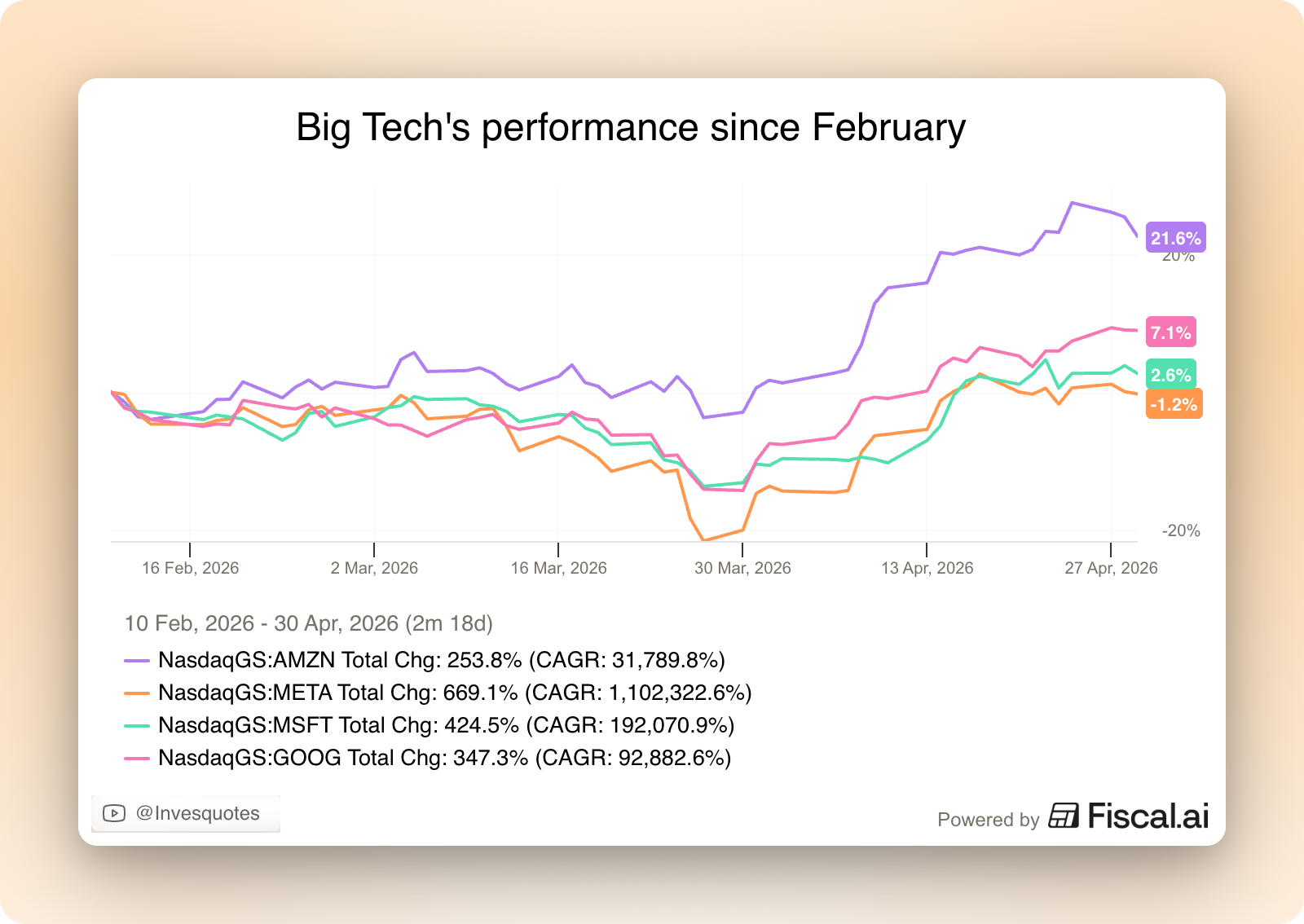

I honestly did not end up doing much (just continued to hold my Amazon shares), but it’s becoming evident that I should’ve and that it’s getting incrementally harder not to own Big Tech. This is what the stocks of Google, Microsoft, Amazon, and Meta have done since the date that article was published (February 10th):

The fate of the Big 4 has been markedly different: only Amazon and Google are up significantly from that date, with Microsoft and Meta falling behind. If one considers that these business are growing at a good pace and are accelerating their top line growth, and the fact that there are no evident signs (at least not yet) that AI investments will deliver sub-par ROIC (more on this later), their risk reward seems to only be getting better (or at least not deteriorating much).

Anyways, this article will review Amazon’s earnings. I hope you understand why I decided to give it the title I did. One could argue that Amazon is one-of-a-kind in terms of being a company that…

Is accelerating its growth at a +$700 billion run rate

Has so much potential growth ahead despite its $700 billion run rate (something unthinkable several years ago)

It’s a very rare/special combo, but one that’s not a coincidence.

Amazon earnings

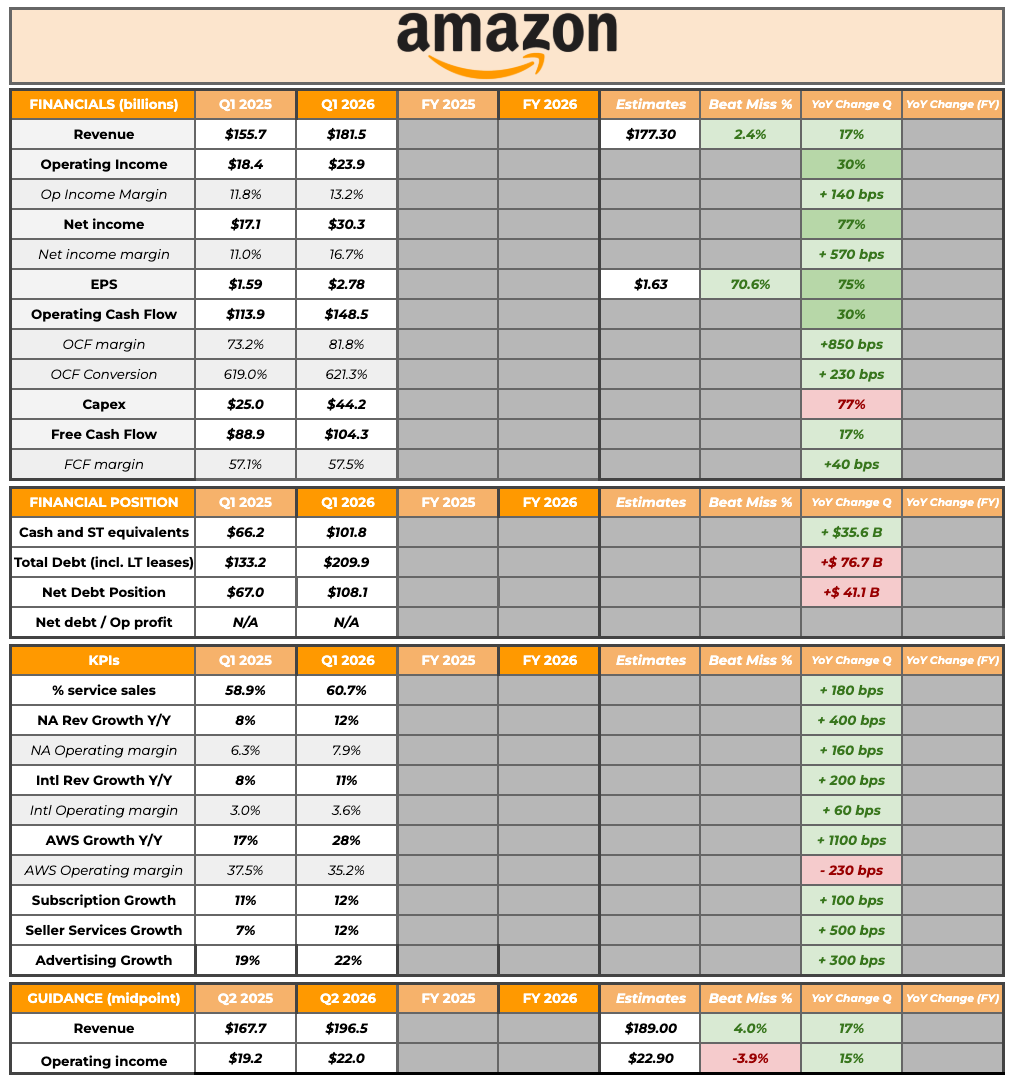

Before jumping into AI and semiconductors (because I am going to mostly talk about this today), let’s take a quick look at Amazon’s summary table:

I believe the table speaks for itself: Amazon delivered a great Q1 across all metrics. The only three reds in the table above need some context. Let’s take the easy one out of the way: the operating income guide came 4% below the market’s expectations. Amazon is well known for sandbagging this metric and I must say that I am surprised that the sell-side has not caught up to this sandbagging. The Q2 top-line guide came considerably above consensus but it’s worth noting that Prime Day this year will take place in Q2 whereas it took place in Q3 last year. I’d imagine part of the consensus took this into account, but no clue.

The other two reds are both related and probably sum up the market’s “concerns”: Capex and AWS’ margins. Capex is not a straightforward one because if one believes that Amazon can invest this Capex at high ROICs, a 77% increase shouldn’t be counted as “red” but actually as “green.” A rational investor would want its companies to invest as much as possible as long the ROIC is worthwhile. The only problem here is that the ROIC on current investments requires some qualitative assessments. The question one should try to answer is:

Will Amazon be able to generate good ROICs on its AWS investments?

Seeing AWS margins come down 250 basis points as Amazon expands capacity is surely fuel for the bears. These might think that it proves they are right, but the reality is that Amazon is investing significantly ahead of being able to monetize its AWS capacity, which ultimately means that margins are not entirely normalized through the investment cycle. Then, bulls could also argue that a 35% operating margin (or even a 30% operating margin) singlehandedly justifies the increased investment Amazon is undertaking. The ultimate reality, though, is that we’ll only know in hindsight.

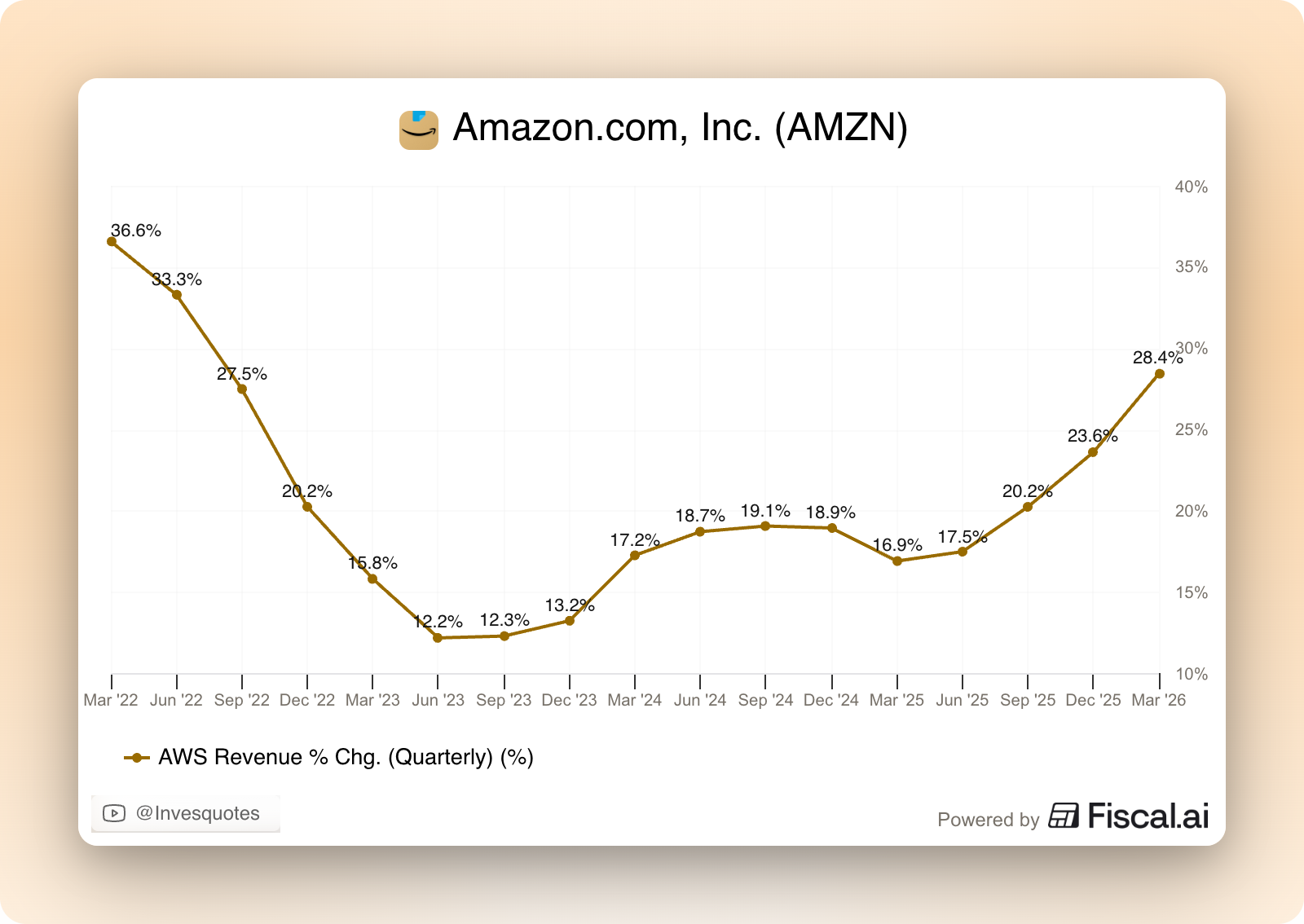

It does seem like Amazon’s business is benefitting from AI in many more ways than investors envisioned. The most straightforward and direct one is AWS (+28% YoY). AI workloads take place in the cloud and hyperscalers are very well positioned to monetize their infrastructure. Not only is Amazon generating direct AI-revenue in AWS (which is growing triple digits), but management also argues that AI is invigorating the “core” business. If you want to jump in the AI train and you are not yet in the cloud, then you got yourself a pretty relevant reason to begin the transition. In short, AI is accelerating the shift to the cloud. What all of this means is that AWS is accelerating at a $150 billion run rate (wow):

Amazon also sized its AWS backlog at $464 billion (including the recently announced +$100 billion deal with Anthropic). Even though this sounds spectacular, I would caution against fixating too much in it. This backlog is based on commitments and not take or pay contracts. This means that, even though demand is still very elevated, it could evaporate in the blink of an eye (not saying it will).

Many people were likely surprised by the fact that Amazon stayed put with the Capex guide despite the rise in memory component pricing. Meta, for example, raised its Capex guide claiming that it was mostly related to higher memory chip pricing (not necessarily increased capacity). With much of the market expecting higher Capex figures as a sign of growing demand and seeing what memory prices have done, one could argue that Amazon “implicitely lowered Capex” while Meta ultimately “maintained” it. I believe Andy Jassy would disagree here as he alluded to front-loading their memory chip investments, but the truth is that this is something that AI bears can hold on to. All this said, the post-2026 commentary by most of the hyperscalers was unidirectional: they expect to spend a lot of Capex on AI over the coming years.

These memory pricing comments, however, are not great news for Nintendo (which dropped considerably again in Japan). It seems like it’s not only margins that might be at stake but also availability (which would be much worse):

These suppliers are prioritizing their very largest customers, which cloud providers are.

Nintendo reports earnings next week, so we’ll see then. In a recent podcast, Jensen Huang (Nvidia’s CEO) mentioned that chip shortages should be, at most, a 2-3 year problem. He also claimed that the real long-term bottleneck is power. This ultimately means that, while not taking place at the best time possible for Nintendo, the chip shortage can prove to be a temporary problem rather than a structural one.

I also thought there were some interesting read-throughs in Amazon’s and Meta’s earnings for a past investment of mine: Adobe. I believe these comments by Amazon and Meta, by the way, hold things for the bears and the bulls. Amazon claimed that creating digital assets is now more accessible than ever, which will lead to a huge rise in advertisers:

You no longer have to take as much time or spend as much money building the creative. I think they’re gonna be a lot more advertisers with the rise of what’s happening in AI.

Meta, on the other hand, claimed that they are seeing traction with the gen AI ad creative tools across their advertisers:

Usage of our ad creative tools is also scaling, with more than 8 million advertisers using at least one of our gen AI ad creative tools and particularly strong adoption among small and medium-sized advertisers.

A bull would say that creative assets are exploding (which is true and part of the Adobe thesis), and a bear would point out that (at least for individuals) the surfaces on which these assets are created might be shifting (might also be true). The more Amazon and Meta continue outgrowing the ads industry, the most likely it is that an independent creative tool gets disintermediated (although one could argue there’s still a long way to go until this happens).

Amazon’s “other” businesses

A growing subset of AWS revenue is in-house chips. Amazon shared some interesting data around its chips business: it’s already at a $20 billion run rate, growing triple digits year over year, and 40% quarter over quarter. The future looks even brighter: commitments for Trainium are already +$225 billion. Andy Jassy also claimed that the business would be at a +$50 billion run rate if Amazon were to be selling Trainium racks to third parties, which they interestingly plan on doing going forward:

On the question of Trainium and the notion of selling racks over time, I do think that’s very much a possibility. There’s a good chance we are going to sell racks over the next couple of years.

Now, I honestly don’t know what competitive advantage will Trainium racks have against Nvidia’s across the “independent” neoclouds (as Trainium’s competitive advantage rests on the fact that the customer’s data is already on AWS), but it’s interesting optionality nonetheless. The good news is that Trainium doesn’t “need to work” with external providers because it’s already delivering measurables benefits to Amazon and its customers:

We expect Trainium will save us tens of billions of dollars of Capex each year and provide several hundred basis points of operating margin advantage versus relying on others’ chips for inference.

Continuing on the topic of AI, I think it’s becoming increasingly evident that AI (and technology in general) is impacting Amazon’s entire business (not just AWS). Take retail. The eCommerce business posted above-average growth and margins (and this despite lower prices YoY). It’s impossible to know for sure, but one could attribute a portion of the accelerated top-line growth to better AI recommendations and initiatives like Rufus or Amazon Now.

One could naturally think (if Meta is any guide) that the Ads business should also improve its performance thanks to AI. Ads growth has not accelerated meaningfully like it has for Meta, but the business continues to grow at +20% rates despite its growing scale. A valid question to make here is whether AI is accelerating the shift to eCommerce by being able to provide better digital experiences that take increased wallet share from shoppers. Based on what we are seeing lately, it surely seems to be the case!

So, while the bears argue that Amazon’s AI investments will not bear fruit, the reality is that Amazon is…

Enjoying accelerated growth across all of its business lines (especially, but not only, AWS)

Seeing margins of the entire business expand while those of AWS remain “stable” considering the investment cycle

Bears will always point to the future as the timeline when they’ll be right, but the facts are not currently supporting their narrative. Will this change? Could be, but nobody has a crystal ball. Now, we should ask ourselves what would happen if bears are right. Let’s assume AI demand eventually cools down. In that scenario, Amazon could potentially stop investing as much in capacity, which would result in significant Free Cash Flow generation. P&L margins would most likely be pressured over the short term, but this would not be something new for Amazon (remember the excess capacity period in eCommerce in the post pandemic period?). Overall, I am not overly worried long-term. I suspect that those who should be more worried are the companies whose business model is currently based on monetizing the capacity that the hyperscalers can’t meet (as those would most likely be the first ones to go).

It’s also worth noting that AI (and everything AI brings with it) is not Amazon’s only optionality. The company an accelerating retail business and initiatives like Amazon Leo. Amazon announced a couple of weeks ago its intention to acquire GlobalStar. GlobalStar gives Amazon two relevant things: scarce direct-to-device capabilities and a strong relationship with Apple (not a small feat considering the installed base).

Now, management also shared several relevant highlights. First, they expect to generate the first Leo commercial revenues in a couple of months. This will be good both for the top line and P&L margins. Amazon is currently incurring P&L expenses related to Leo despite this being a “pre-revenue” initiative. This changes in a couple of months. I am not an expert on satellite networks, but I do believe that Leo comes with some differentiation points unique to Amazon (among the other providers):

Just the combination of Leo with the leading cloud in the world in AWS is very compelling to enterprises and to governments.

All in all, outstanding earnings by Amazon which trades at an EV/EBIT of around 35 while it accelerates its growth and margin expansion and in the verge of yet another revenue stream (Leo). Does Amazon seem incredibly cheap at current levels? No, it doesn’t. Is there enough optionality to support the current valuation? I believe there is.

Have a great day,

Leandro

Amazon has built a massive custom silicon chip business to power its scaling AI infrastructure challenging Nvidia and AMD. Custom Trainium silicon exposure gives an advantage over expensive chip stocks. Historically, heavy investment phases are followed by explosive cash flow growth driven by internal operating leverage. I expect a 20%+ from here per my DCF. See more here: https://freecashflowcompounder.substack.com/p/portfolio-valuation-as-of-may-31