A new position, Mag 5 Earnings, Adobe’s Insider Sales, and Flawed Narratives (NOTW#90)

Best Anchor Stocks has a partnership with Fiscal.ai (the research platform I personally use), through which you can enjoy a 15% discount on any plan. Use this link to claim yours! You’ll find KPIs, Copilot (a ChatGPT focused on finance) and the best UX:

You can read this article (almost) entirely for free. If you like what you read, consider becoming a paid member to get access to…

All in-depth reports (15 companies profiled thus far, and growing)

Earnings follow-ups

Other investment related content

A community of like-minded investors

Complete access to my portfolio and transactions

Occasional webinars

The in-depth reports of Stevanato and Deere are free to read to gauge the quality of the research.

Join today:

It was an interesting week in the market as the Mag 5 (MSFT, GOOG, META, AMZN, and AAPL) reported earnings in the space of 2 days. These companies’ earnings can be bifurcated in two distinct groups, but I’d imagine that a lot of people expected a much more volatile week than we got. Markets are still trading at ATHs and the music seems to have some legs (this might age poorly!).

Without further ado, let’s get on with it.

Articles of the week

I published two articles this week, both earnings digests. The first one was Texas Instruments’ Q1 update.

Confirmed data center + inflection play

Texas Instruments delivered an outstanding quarter last week. One doesn’t have to look much further than what the company delivered against expectations…

The company reported outstanding earnings (despite the forecasts of many semiconductor “experts”) and rose to fresh ATHs. It has been a rocky path, but shares have finally responded.

The second article of the week was Amazon’s Q1 earnings update.

Acceleration inbound and optionality abound

Last quarter, I concluded my Amazon Q4 update (where I also made the case for Big Tech) with the following:

The company again reported a significant acceleration, but the acceleration was not isolated to AWS this time. There are reasons to believe that AI is positively impacting each and every one of Amazon’s operating businesses, to which we must add a new revenue stream coming live later this year.

Market Overview

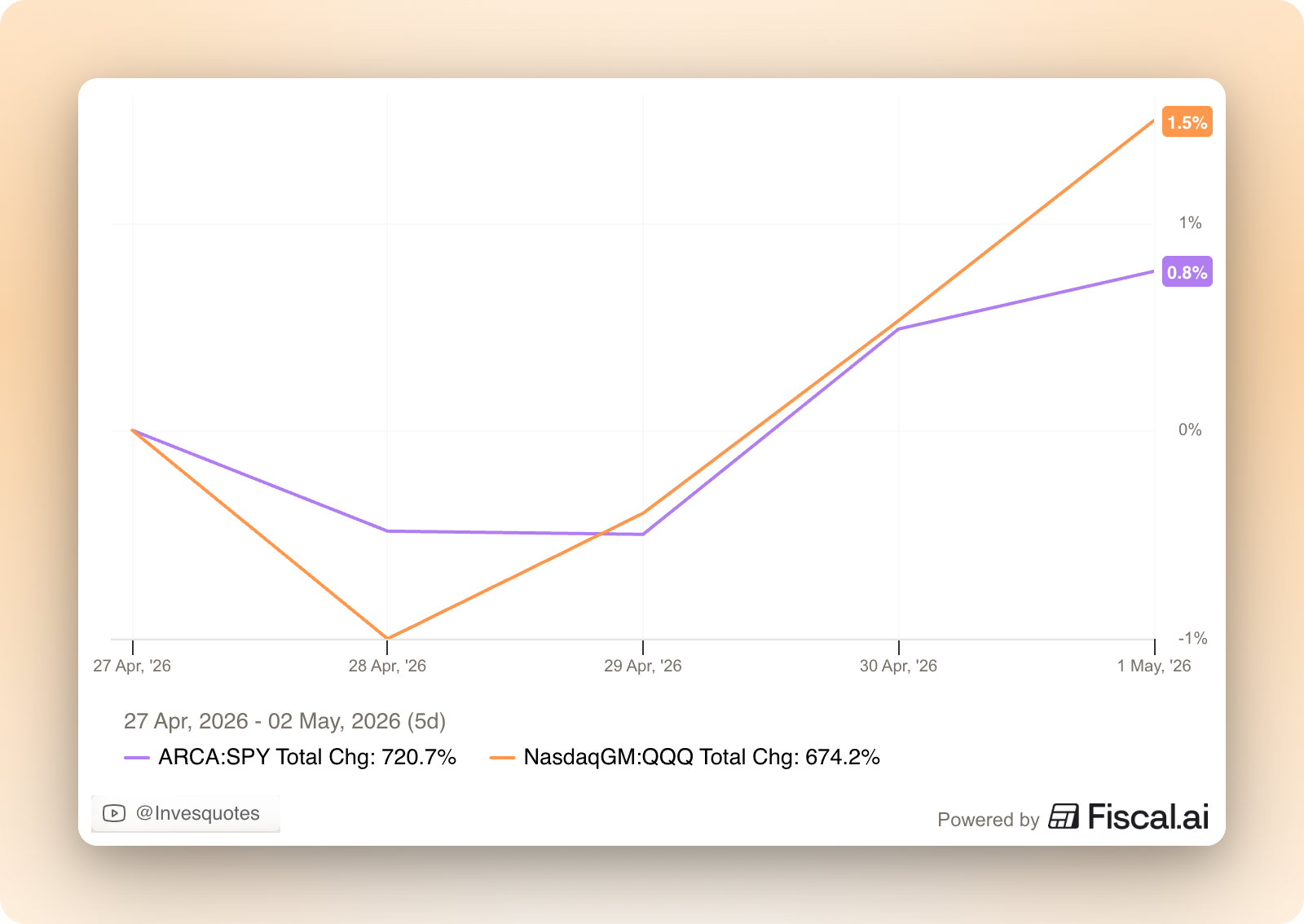

Both indices were up again this week (surprised? ha):

It was a pretty relevant week for financial markets. The Mag 5 reported earnings: Microsoft, Google, Meta, Amazon, and Apple. Someone could’ve claimed that this was a “crucial” week for financial markets, but the reality is that it was a pretty calm week all things considered. Microsoft, Google, Meta, and Amazon reported somewhat “similar” earnings in the sense that they are all spending significant Capex on AI and that they plan to continue doing so in the years to come. Many of these companies claim that AI is “a revolution unlike any other” and that the Capex is money well spent/invested. While this is something that we’ll only know in hindsight, I don’t think that all investor skepticism around this Capex is misguided.

Apple, on the other hand, reported earnings in line with what everyone expected from them (in the Capex sense): very little Capex and strong returns of capital to shareholders. The strategies of Apple and the rest of the Mag 5 are strikingly different, but there’s no denying that Apple holds a large chunk of the hardware through which AI is distributed. Tim Cook claimed that the Mac Mini has seen heightened demand from AI and I believe that Apple is raising prices (maybe led by higher demand as well as higher memory costs). So, Apple is not spending the Capex but it’s “clearly” benefiting from AI. Who will be right long term, Apple or the rest of the Mag 5? I believe that this question is a tad useless because both can be right in owning different parts of the value chain. We’ll see.

Even though this week was important for markets in general, the real important weeks for my portfolio are the next two (especially the one that’s coming up right now). I have around 40% of my portfolio reporting next week and I am excited for earnings season (this might age poorly!). I believe my two top positions will put their respective narratives to (hopefully) rest, although I must say that, for my top position, there are already significant signs that point to a flawed narrative (more about this in the company-specific news section).

In other news, Adobe’s CEO, Shantanu Narayen, sold around $18 million worth of shares this week:

A couple of weeks ago, I published the following on X:

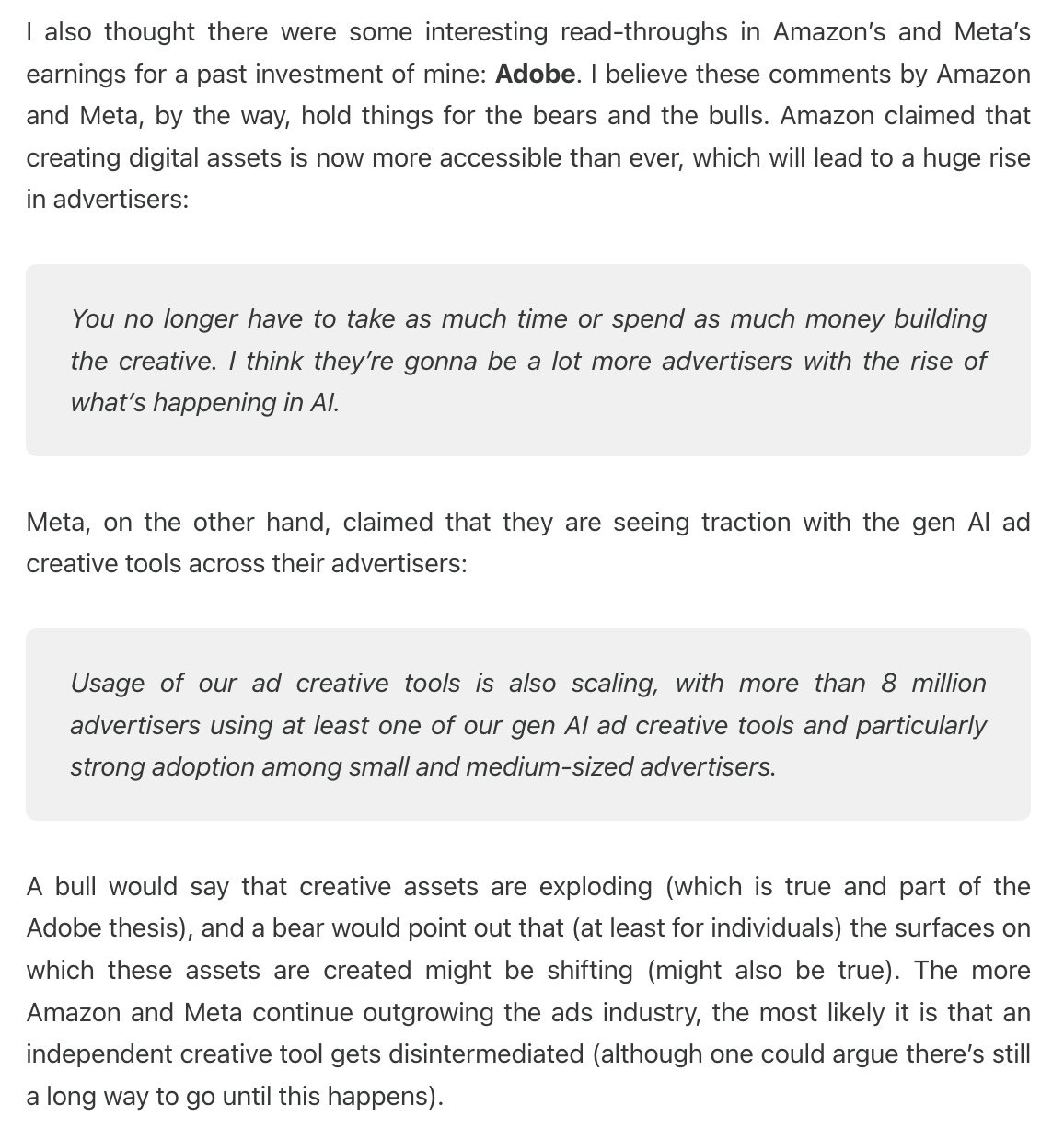

I don’t want to be overly critical on Adobe (as I don’t own it anymore and it can appear to be opportunistic), but this is precisely what I discussed in my post. It might be great that Adobe’s management is repurchasing shares at historical low valuations (we’ll only know in hindsight), but a much stronger sign of management confidence would be if insiders were also putting their money (not yours) where their mouth is. The reality is that Adobe has not seen a single insider purchase over the last year and that the CEO just filed to sell $18 million worth of stock at the historical low valuation (plus the fact that he left without succession, which seemed weird). In my most recent Amazon update I shared two interesting quotes I found in Meta’s and Amazon’s earnings call that “impact” Adobe. There’s food for both the bulls and the bears:

Software had a relatively good day on Friday after Atlassian reported what appeared to be great earnings. Its stock was up almost 30% and the IGV was up 3%. Does this invalidate the fact that Adobe might be in “trouble” due to AI? No, the reality is that, within software, there will be companies that thrive thanks to AI and others that disappear (not claiming Adobe will be in the latter group!). What I do think that many of these SaaS stocks reactions prove is that the market has thrown the baby out with the bathwater and that there are likely interesting opportunities in the sector.

The industry map was mixed this week, coherent with the fact that we are in earnings season:

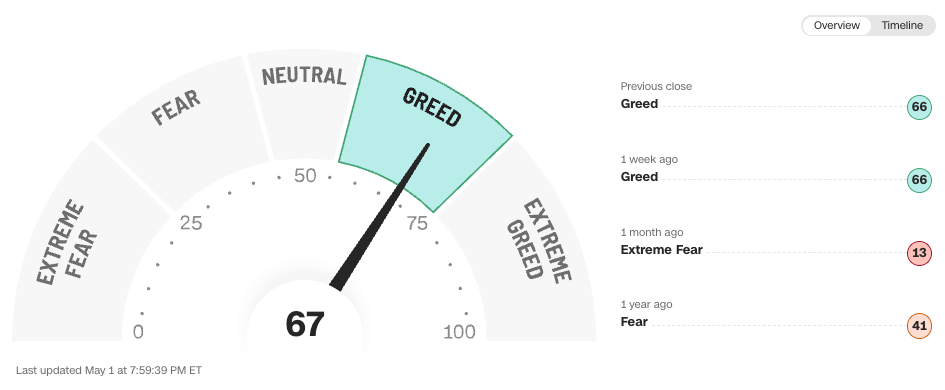

The fear and greed index remained in greed territory:

One trim and one new position

I made two moves this week. First, I decided to trim one of my long-standing positions. The stock had risen to the #2 spot in my portfolio due to its great performance, and I was not comfortable with that at the current valuation. Peter Lynch would say I “trimmed the flowers” and he might be right, but I believe there are ample opportunities to deploy this capital in.

I also started a fresh new position which I expect to hold over the long term. Management is very aligned with shareholders on this one and has the track record to back their confidence in the model: